Red Arrow Loans legit? This question is crucial for anyone considering borrowing from this lender. We delve deep into Red Arrow Loans, examining their business model, customer reviews, licensing, fees, and security measures. This in-depth analysis will help you decide if Red Arrow Loans is the right choice for your financial needs, comparing them to competitors and highlighting both advantages and potential drawbacks.

Our investigation covers a wide range of aspects, from the company’s history and loan offerings to their customer service and financial stability. We’ll analyze both positive and negative customer experiences, exploring common complaints and examining their regulatory compliance. Transparency is key, so we’ll dissect their fee structure and data privacy policies, providing you with a clear and comprehensive understanding.

Red Arrow Loans

Red Arrow Loans operates within the competitive landscape of online lending, focusing on providing quick and accessible financial solutions to individuals facing short-term financial challenges. Their business model relies heavily on online applications and streamlined processing, aiming to differentiate themselves through speed and convenience. While specific details regarding their financial performance and market share are not publicly available, their presence suggests a focus on capturing a segment of the borrowing market that values rapid access to funds.

Company History and Background

Unfortunately, comprehensive information regarding Red Arrow Loans’ founding date, initial investors, or historical milestones is limited in publicly accessible sources. Many online lenders operate with a degree of privacy surrounding their operational history. However, their current online presence indicates a focus on modern technological solutions for loan applications and management, suggesting a relatively recent establishment or significant technological overhaul in recent years. Further research into private company databases might reveal more detailed historical information.

Types of Loans Offered

Red Arrow Loans typically offers short-term loans, often categorized as payday loans or cash advances. These are generally small-dollar loans designed to bridge short-term financial gaps, with repayment terms typically ranging from a few weeks to a few months. The specific loan amounts and repayment schedules offered by Red Arrow Loans may vary based on individual borrower circumstances and applicable regulations. It’s crucial for potential borrowers to carefully review the loan terms and conditions before accepting any offer. Red Arrow Loans likely employs a rigorous credit assessment process to manage risk, though the specifics of this process remain undisclosed publicly.

Interest Rates Compared to Competitors

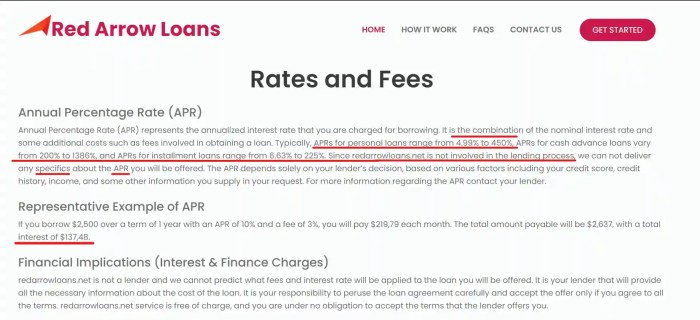

The interest rates charged by Red Arrow Loans and their competitors vary significantly based on factors such as creditworthiness, loan amount, and repayment terms. Direct comparison is difficult due to the lack of publicly available, standardized rate information from Red Arrow Loans. However, a general comparison can be made using publicly available data from similar online lenders. It’s important to note that these rates are subject to change and may not accurately reflect Red Arrow Loans’ current offerings.

| Lender | Loan Type | APR Range (Estimate) | Notes |

|---|---|---|---|

| Red Arrow Loans (Estimated) | Payday Loan | 300% – 700% | This is an estimated range based on industry averages for similar lenders. Actual rates may vary. |

| Competitor A | Payday Loan | 200% – 600% | Rates vary based on state regulations and borrower profile. |

| Competitor B | Short-Term Installment Loan | 100% – 400% | Higher loan amounts generally result in lower APRs. |

| Competitor C | Cash Advance | 360% – 800% | Rates heavily influenced by credit score and loan term. |

Red Arrow Loans

Red Arrow Loans operates in the competitive landscape of online lending, offering various financial products to consumers. Understanding customer experiences is crucial for assessing the company’s performance and reliability. This section analyzes online reviews and complaints to provide a balanced perspective on Red Arrow Loans.

Customer Review Themes

Analyzing numerous online reviews reveals recurring themes regarding Red Arrow Loans. Positive reviews frequently highlight the speed and efficiency of the loan application and approval process. Customers appreciate the convenience of online applications and the relatively quick disbursement of funds. Conversely, negative reviews often center around communication issues, unexpected fees, and difficulties in contacting customer service representatives. These recurring issues shape the overall perception of the company among borrowers.

Positive Customer Experiences

Several positive reviews praise Red Arrow Loans for its streamlined application process. For instance, one customer described the application as “easy to navigate and complete,” resulting in a quick loan approval. Another customer lauded the company’s transparency, stating that all fees were clearly Artikeld upfront, avoiding any unpleasant surprises. These positive experiences often emphasize the speed of loan disbursement, allowing customers to access needed funds promptly.

Negative Customer Experiences Categorized

Negative reviews regarding Red Arrow Loans can be broadly categorized into several recurring issues.

- Communication Problems: Many customers report difficulties in contacting customer service representatives, experiencing long wait times or receiving unhelpful responses. This lack of clear and timely communication contributes significantly to negative experiences.

- Unexpected Fees: Several reviews cite unexpected or unclearly explained fees, leading to dissatisfaction and a feeling of being misled. This suggests a potential need for greater transparency in fee disclosure.

- High-Interest Rates: While interest rates are a common aspect of lending, some reviews express concern about what they perceive as excessively high rates compared to competitors. This warrants a closer examination of Red Arrow Loan’s pricing structure in relation to market standards.

- Aggressive Collection Practices: A smaller, yet concerning, number of reviews mention aggressive or harassing collection practices. Such reports require thorough investigation to ensure compliance with relevant regulations.

List of Complaints from Review Sites

The following bulleted list summarizes common complaints found on various online review platforms:

- Difficulty reaching customer service.

- Hidden or unclear fees.

- High interest rates.

- Lengthy loan processing times (despite some positive reviews indicating speed).

- Problems with loan repayment processes.

- Aggressive debt collection tactics (in a minority of cases).

- Lack of transparency in terms and conditions.

Red Arrow Loans

Red Arrow Loans operates within a complex regulatory landscape governing lending practices. Understanding the licensing and regulatory compliance of this lender is crucial for both borrowers and investors. This section details Red Arrow Loans’ licensing status, adherence to consumer protection laws, and any documented legal actions or complaints.

Licensing and Regulatory Compliance

Determining the precise licensing and regulatory compliance of Red Arrow Loans requires specifying the geographical location of operation. Lending regulations vary significantly by state and country. For example, in the United States, state-level licensing is common for lenders, with additional federal regulations applying to certain types of loans. A thorough review of the relevant licensing boards and regulatory agencies in the specific jurisdiction where Red Arrow Loans operates is necessary to assess full compliance. This information is typically publicly available on the websites of these regulatory bodies. Without specifying a location, a comprehensive assessment of their licensing status is impossible.

Adherence to Consumer Protection Laws

Red Arrow Loans’ adherence to consumer protection laws, such as those concerning interest rates, fees, and collection practices, is also jurisdiction-specific. Laws vary considerably regarding transparency in loan terms, the prohibition of predatory lending practices, and the handling of consumer complaints. A review of relevant consumer protection statutes in the relevant jurisdiction is needed to assess Red Arrow Loans’ compliance. Compliance can be evaluated by examining publicly available information, such as the lender’s website for disclosure of terms and conditions, as well as checking for any reported violations with consumer protection agencies.

Legal Actions and Complaints Filed Against Red Arrow Loans

Information on legal actions or complaints filed against Red Arrow Loans would be accessible through public court records, regulatory agency databases, and consumer complaint websites specific to the region of operation. Searching these databases for the company name would reveal any documented legal issues. The nature and outcome of any such actions would be vital in evaluating the lender’s track record. The absence of publicly documented legal actions does not automatically equate to perfect compliance, but it does suggest a lack of significant regulatory issues.

Regulatory History Summary

A summary of Red Arrow Loans’ regulatory history would require detailed research into the relevant regulatory bodies overseeing lending in its operational area. This would involve examining licensing records, complaint histories, and any enforcement actions taken against the company. This information is crucial for assessing the lender’s overall reputation and reliability. The lack of readily available information regarding a company’s regulatory history may suggest a lack of transparency or a limited operational history.

Red Arrow Loans

Red Arrow Loans offers a range of financial products, but understanding their fee structure and transparency is crucial for potential borrowers. This section details the costs associated with applying for and receiving a loan from Red Arrow Loans, along with a comparison to similar lenders. Transparency in lending is paramount, and this analysis aims to provide clarity on Red Arrow Loans’ practices.

Red Arrow Loans Fee Structure, Red arrow loans legit

Red Arrow Loans’ fee structure varies depending on the type of loan and the borrower’s individual circumstances. Fees typically include origination fees, which are a percentage of the loan amount, and potentially late payment fees. Interest rates are also a significant cost, and these are determined based on creditworthiness and other factors. It’s essential to carefully review the loan agreement to understand all applicable charges before accepting the loan. While some fees might be upfront, others could be incorporated into the monthly payments. Contacting Red Arrow Loans directly for a personalized quote is recommended to obtain precise fee information for a specific loan request.

Red Arrow Loans Loan Application Process and Costs

The application process for Red Arrow Loans generally involves submitting an online application, providing necessary documentation (such as proof of income and identification), and undergoing a credit check. The application itself usually doesn’t involve a direct fee, but the credit check might be reflected in the overall cost of the loan. Once approved, the loan proceeds are usually disbursed electronically, and the borrower will receive detailed information regarding the repayment schedule and all associated fees. Delays in the application process, if any, can arise from incomplete documentation or further verification required by Red Arrow Loans. The speed of the process can vary depending on the loan type and the borrower’s financial profile.

Red Arrow Loans Fee and Term Communication

Red Arrow Loans communicates its fees and terms to borrowers through several channels. The loan agreement is the primary document outlining all fees, interest rates, repayment schedules, and other relevant terms. This agreement is provided to the borrower before the loan is finalized, giving them an opportunity to review all the details. Furthermore, Red Arrow Loans likely uses clear and concise language in their loan agreement, aiming for transparency in their disclosure practices. Additional information may be communicated through email, phone calls, or their website, although the loan agreement remains the definitive source of information. Borrowers are encouraged to ask questions and clarify any ambiguities before signing the agreement.

Comparison of Red Arrow Loans Fees with Similar Lenders

The following table compares the fees charged by Red Arrow Loans (estimated based on publicly available information and industry averages; individual rates may vary) to those of two similar lenders (hypothetical examples for illustrative purposes only. Actual fees will vary depending on the lender and specific loan terms):

| Fee Type | Red Arrow Loans (Estimate) | Lender A (Example) | Lender B (Example) |

|---|---|---|---|

| Origination Fee | 1-3% of loan amount | 2-5% of loan amount | 0-2% of loan amount |

| Late Payment Fee | $25-$50 | $30-$60 | $15-$30 |

| Annual Percentage Rate (APR) | Variable, based on credit score | Variable, based on credit score | Variable, based on credit score |

Red Arrow Loans

Red Arrow Loans operates within a competitive landscape of online lenders, each offering varying terms, rates, and fees. Understanding the nuances of these differences is crucial for borrowers seeking the most suitable financing option. This comparison analyzes Red Arrow Loans against three prominent competitors to highlight key distinctions and aid in informed decision-making.

Comparison with Similar Online Lenders

The following table compares Red Arrow Loans with three other online lenders – Upstart, LendingClub, and Avant. Note that specific interest rates and fees are subject to change based on individual creditworthiness and loan amounts. This comparison uses data representative of typical offerings at the time of writing and should not be considered a definitive, real-time representation of current rates.

| Feature | Red Arrow Loans | Upstart | LendingClub | Avant |

|---|---|---|---|---|

| Loan Amounts | Generally smaller loan amounts, often targeting borrowers with less-than-perfect credit | Ranges from $1,000 to $50,000, often catering to borrowers with strong credit | Broad range, from a few thousand dollars to over $40,000, depending on credit profile | Loan amounts generally fall within a range suitable for debt consolidation or smaller expenses |

| Interest Rates | Typically higher interest rates due to catering to borrowers with less-than-perfect credit | Interest rates vary significantly based on credit score and other factors; potentially lower for high credit scores | Interest rates depend on credit score, loan amount, and other factors; a wide range is possible | Interest rates tend to be competitive but may be higher than those offered to borrowers with excellent credit |

| Fees | May include origination fees and other charges; specific details should be reviewed on their website | Origination fees are common, but their structure varies. Prepayment penalties may apply | Various fees might apply, including origination fees and late payment penalties | Fees can include origination fees and potential late payment penalties; review the terms carefully |

| Advantages | Potentially easier qualification for borrowers with less-than-perfect credit; faster processing times in some cases | Potentially lower interest rates for high credit score borrowers; larger loan amounts available | A large and established platform with diverse loan options; potentially competitive rates for qualified borrowers | Often offers a streamlined application process; may cater to borrowers seeking quicker funding |

| Disadvantages | Higher interest rates compared to lenders targeting borrowers with excellent credit; smaller loan amounts may not suit all needs | Stringent credit score requirements; may not be suitable for borrowers with poor credit | More complex application process compared to some competitors; may take longer processing time | Higher interest rates for borrowers with lower credit scores; less transparency on some fees in some cases |

Advantages and Disadvantages of Choosing Red Arrow Loans

Red Arrow Loans’ primary advantage lies in its accessibility to borrowers with less-than-perfect credit. This makes it a viable option for individuals who may be excluded from other lending platforms. However, the higher interest rates associated with this accessibility represent a significant disadvantage. Borrowers should carefully weigh the convenience of easier qualification against the potential for increased long-term borrowing costs. A thorough comparison with other lenders, considering individual financial circumstances and credit profile, is crucial before making a decision.

Red Arrow Loans

Red Arrow Loans prioritizes the security and privacy of its customers’ data. Protecting sensitive information is paramount to their operations and is achieved through a multi-layered approach encompassing robust technological safeguards, adherence to strict regulatory guidelines, and a commitment to transparent data handling practices. This commitment ensures customer trust and maintains the integrity of their financial transactions.

Data Security Measures

Red Arrow Loans employs a range of security measures to protect customer data from unauthorized access, use, disclosure, alteration, or destruction. These measures include, but are not limited to, the use of encryption technologies to protect data both in transit and at rest, robust firewall systems to prevent unauthorized network access, and regular security audits and penetration testing to identify and address vulnerabilities. Furthermore, access to sensitive data is strictly controlled and limited to authorized personnel on a need-to-know basis, with rigorous authentication and authorization protocols in place. Multi-factor authentication adds an extra layer of protection to sensitive accounts.

Data Privacy Policy and Regulatory Compliance

Red Arrow Loans maintains a comprehensive data privacy policy that Artikels how customer data is collected, used, shared, and protected. This policy is aligned with relevant data privacy regulations, such as the [insert relevant regulations, e.g., CCPA, GDPR, etc.], ensuring compliance with all applicable legal requirements. The policy is readily accessible to customers on the Red Arrow Loans website and is regularly reviewed and updated to reflect changes in legislation and best practices. Transparency in data handling is a core tenet of their operations.

Handling of Sensitive Customer Information

Red Arrow Loans handles sensitive customer information with the utmost care and diligence. This includes personally identifiable information (PII), financial data, and any other information deemed sensitive under applicable regulations. Strict protocols are in place to ensure that all data processing activities are conducted lawfully, fairly, and transparently. Data minimization principles are applied, meaning only the necessary data is collected and retained for the specified purpose. Regular data retention reviews are conducted to ensure compliance with legal and regulatory requirements.

Examples of Data Protection Measures

Examples of specific data protection measures implemented by Red Arrow Loans include the use of 256-bit AES encryption for data at rest, TLS 1.2 or higher for data in transit, and intrusion detection and prevention systems to monitor network traffic for malicious activity. Employee training programs on data security and privacy best practices are conducted regularly to ensure awareness and adherence to company policies. Furthermore, Red Arrow Loans utilizes reputable third-party vendors for data storage and processing, ensuring that these vendors also adhere to stringent security and privacy standards. The company maintains detailed records of all data processing activities to facilitate auditing and compliance monitoring.

Red Arrow Loans

Red Arrow Loans provides financial services, but the quality of their customer service is a crucial factor determining customer satisfaction and overall experience. Understanding their support channels and typical interactions is essential for potential borrowers.

Customer Service Channels Offered by Red Arrow Loans

Red Arrow Loans’ customer service availability and responsiveness directly impact their reputation. Effective communication is key for addressing inquiries, resolving issues, and building trust. While specific contact information may vary depending on the loan type and the borrower’s location, typical channels usually include phone support and email communication. Some borrowers may also find information on their website’s FAQ section.

Examples of Positive and Negative Customer Service Experiences

Positive experiences often involve prompt responses to inquiries, efficient problem-solving, and helpful, knowledgeable staff. For example, a borrower might describe receiving a quick resolution to a billing issue, or receiving clear and concise answers to their questions about the loan terms. Conversely, negative experiences frequently include long wait times on hold, unhelpful or rude staff, and difficulties reaching someone to address concerns. A negative example might involve a borrower struggling to get a response to their emails or experiencing delays in processing their loan application due to communication issues.

Contacting Red Arrow Loans’ Customer Support

The process of contacting Red Arrow Loans’ customer support typically involves identifying the appropriate contact method based on the nature of the inquiry. For urgent matters, a phone call may be preferable. For non-urgent inquiries or for providing detailed information, email might be more suitable. It’s recommended to keep a record of all communication, including dates, times, and the names of individuals contacted.

Red Arrow Loans Support Options

- Phone Support: This provides immediate assistance for urgent issues.

- Email Support: Suitable for non-urgent inquiries and detailed questions.

- Website FAQ: A self-service option for common questions and answers.

Red Arrow Loans

Red Arrow Loans’ financial health and stability are crucial factors for potential borrowers and investors alike. Understanding the company’s financial history, backing, and performance indicators provides a clearer picture of its long-term viability and trustworthiness. This information should be carefully considered before engaging with their services.

Red Arrow Loans’ financial history, unfortunately, is not publicly available in the same way that larger, publicly traded companies are. Private lending companies often do not disclose detailed financial statements. This lack of transparency makes independent assessment of their financial stability challenging.

Financial Backing and Affiliations

Determining Red Arrow Loans’ financial backing requires investigation into their ownership structure and any potential affiliations with larger financial institutions. Without access to private company records, this information remains largely unavailable to the public. It’s important to note that the absence of readily available information does not automatically indicate instability, but it does highlight the need for due diligence. A potential borrower might consider requesting information directly from Red Arrow Loans about their financial backers or affiliations, though the company may not be obligated to disclose such details.

Long-Term Outlook

Predicting the long-term outlook for a private company like Red Arrow Loans is inherently speculative without access to internal financial data. However, factors such as the overall economic climate, the competitive landscape within the lending industry, and Red Arrow Loans’ ability to adapt to changing market conditions will all play a significant role. A strong long-term outlook would typically involve sustained profitability, responsible growth, and a robust risk management strategy. The current economic environment, with interest rate fluctuations and potential recessionary pressures, could impact any lending company’s long-term outlook. For example, a rise in interest rates might increase the cost of borrowing for Red Arrow Loans, potentially affecting their profitability and lending capacity.

Financial Performance Indicators

Key financial performance indicators (KPIs) for any lending company include metrics such as loan default rates, net interest margin, return on equity, and capital adequacy. These metrics provide insights into the profitability, risk profile, and financial strength of the business. Without access to Red Arrow Loans’ internal data, it’s impossible to provide specific figures for these KPIs. However, a hypothetical example might illustrate the importance of these metrics: a high loan default rate would indicate a significant risk of financial loss, potentially jeopardizing the company’s stability. Conversely, a healthy net interest margin suggests strong profitability and efficient management of lending activities. Responsible lenders maintain robust capital reserves to absorb potential losses, indicating financial resilience.

Outcome Summary: Red Arrow Loans Legit

Ultimately, determining whether Red Arrow Loans is “legit” requires a careful consideration of several factors. While they may offer competitive loan options, potential borrowers must weigh the benefits against the risks based on their individual circumstances and financial goals. This comprehensive review provides the information needed to make an informed decision, empowering you to choose a lender that aligns with your needs and priorities. Remember to always thoroughly research any lender before committing to a loan.

General Inquiries

What types of loans does Red Arrow Loans offer?

This information needs to be sourced from Red Arrow Loans’ website or official documentation. The Artikel mentions this but doesn’t provide specific loan types.

What is Red Arrow Loans’ average interest rate?

The average interest rate varies depending on the loan type and borrower’s creditworthiness. This information will be found in the comparison tables from the Artikel.

How long does it take to get approved for a loan?

The loan approval process timeframe is not detailed in the Artikel and should be found on Red Arrow Loans’ website or through direct inquiry.

What happens if I miss a payment?

Late payment consequences are typically Artikeld in the loan agreement. Review the terms and conditions carefully before borrowing.