SEFCU loan rates are a crucial factor for anyone considering borrowing from this credit union. Understanding these rates, how they’re determined, and what influences them is key to making informed financial decisions. This guide delves into the specifics of SEFCU’s loan offerings, providing a comprehensive overview of their various loan types, associated interest rates, and the impact of factors like credit score on your overall cost. We’ll also explore SEFCU’s transparency regarding rates and compare them to those of competing institutions, equipping you with the knowledge needed to secure the best possible loan terms.

We’ll examine the calculation methods used by SEFCU, explore associated fees, and dissect the impact of various promotions and special offers. By the end, you’ll have a clear understanding of SEFCU loan rates and how to navigate the process of securing a loan.

Understanding SEFCU Loan Rates

SEFCU, or the Schenectady County Employees Federal Credit Union, offers a range of loan products with varying interest rates. Understanding these rates is crucial for potential borrowers to make informed financial decisions and secure the most suitable loan option. Factors such as credit score, loan amount, and loan type significantly impact the final interest rate offered. This analysis will clarify the factors that influence SEFCU’s loan rate determination and provide a comparison with competing institutions.

SEFCU Loan Rate Determination

Several key factors influence the interest rates SEFCU assigns to its loans. These include the borrower’s creditworthiness, as assessed by their credit score and history; the loan amount itself, with larger loans potentially carrying higher rates; the loan term, with longer repayment periods often resulting in higher overall interest; the type of loan, as different loan products carry different risk profiles; and prevailing market interest rates, which affect the overall cost of borrowing for financial institutions. A higher credit score generally translates to a lower interest rate, reflecting a lower perceived risk for the lender. Similarly, a shorter loan term reduces the lender’s risk and can lead to a lower interest rate.

Types of SEFCU Loans and Associated Interest Rates

SEFCU offers a variety of loan products, each with its own rate structure. These include auto loans, often used for purchasing new or used vehicles; mortgages, for financing the purchase of a home; personal loans, designed for various personal expenses; and home equity loans, which utilize the equity in a homeowner’s property as collateral. The interest rates for each loan type vary based on the factors Artikeld above. For example, auto loan rates may be lower than personal loan rates due to the presence of collateral (the vehicle). Specific interest rates are not publicly listed and are determined on a case-by-case basis after reviewing the applicant’s financial information. Contacting SEFCU directly is necessary to obtain a personalized rate quote.

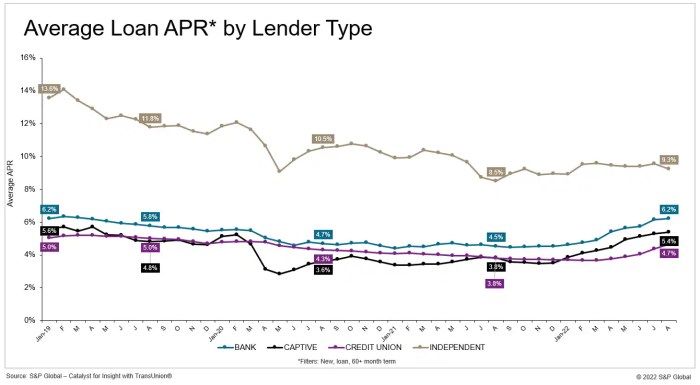

Comparison of SEFCU Loan Rates with Competitors

Direct comparison of SEFCU loan rates with competitors requires obtaining current rate quotes from each institution. Rate quotes are dynamic and vary based on individual circumstances. However, a hypothetical comparison can illustrate the general principles involved. The table below presents a simplified example and should not be considered definitive. Actual rates will vary.

| Loan Type | SEFCU (Hypothetical) | Competitor A (Hypothetical) | Competitor B (Hypothetical) |

|---|---|---|---|

| Auto Loan (New) | 4.5% – 7.5% APR | 4.0% – 8.0% APR | 5.0% – 7.0% APR |

| Personal Loan | 8.0% – 15.0% APR | 7.5% – 16.0% APR | 9.0% – 14.0% APR |

| Mortgage (30-year fixed) | 5.5% – 7.0% APR | 5.0% – 6.5% APR | 6.0% – 7.5% APR |

SEFCU Loan Rate Transparency

SEFCU’s communication of loan rates to its members is a crucial aspect of its service. Transparency in this area fosters trust and allows members to make informed financial decisions. This section examines SEFCU’s methods for disseminating loan rate information, its accessibility, potential areas for improvement, and proposes a user-friendly infographic to clarify the loan rate structure.

SEFCU employs multiple channels to communicate its loan rates. These include its official website, in-person interactions with loan officers at branches, and potentially through marketing materials such as brochures and email campaigns. The website, ideally, should provide detailed rate information for various loan types, including personal loans, auto loans, mortgages, and home equity lines of credit. In-person consultations offer members the opportunity to discuss their specific financial situations and receive personalized rate quotes. However, the consistency and comprehensiveness of information across all channels are key factors in determining overall transparency.

SEFCU’s Online and In-Person Loan Rate Information

SEFCU’s website should ideally provide readily accessible rate information. A dedicated section clearly outlining interest rates, APRs (Annual Percentage Rates), and any associated fees for different loan products is essential. This information should be presented in a clear, concise, and easily understandable format, avoiding jargon. In-person access to this information should be equally straightforward, with loan officers trained to provide accurate and complete information. Ideally, rate sheets or brochures should be readily available in branches to supplement the verbal explanation. Inconsistencies between online and in-person information would indicate a lack of transparency and potentially undermine member trust.

Potential Areas for Improvement in SEFCU Loan Rate Transparency

While SEFCU may already have mechanisms in place to communicate loan rates, potential improvements could include creating a comprehensive, frequently updated online loan rate calculator. This calculator would allow members to input their specific financial details and receive a personalized estimate of their potential loan rate. Another area for improvement is providing clearer explanations of the factors influencing loan rates, such as credit score, loan amount, and loan term. This could help members understand how they can improve their chances of securing a favorable rate. Finally, proactively communicating changes in loan rates through email or SMS alerts to existing members would enhance transparency and keep members informed.

Infographic Design: Understanding SEFCU Loan Rates

The infographic would use a visually appealing and easily digestible format to explain SEFCU’s loan rate structure. The title would be “Understanding Your SEFCU Loan Rate.” The infographic would be divided into clear sections. The first section would explain the key terms: APR, interest rate, loan term, and loan amount. Each term would be defined concisely with a simple example. The second section would illustrate how these factors interact to determine the final loan rate. A simple chart or graph could visually represent the relationship between these factors and the resulting rate. For example, a line graph could show how the interest rate changes with varying credit scores, keeping other factors constant. A third section could present examples of loan rate scenarios. For example: “A $10,000 loan with a 750 credit score might have a 5% APR,” and “A $20,000 loan with a 650 credit score might have a 7% APR.” The infographic would conclude with a call to action, encouraging members to visit the SEFCU website or contact a loan officer for more information. The overall design should utilize clear fonts, a consistent color scheme, and visually engaging icons to enhance understanding and memorability. The use of color-coding to highlight key information would also improve readability.

Impact of Credit Score on SEFCU Loan Rates

Your credit score significantly influences the interest rate SEFCU offers on loans. A higher credit score generally translates to a lower interest rate, resulting in lower monthly payments and less overall interest paid over the life of the loan. Conversely, a lower credit score can lead to higher interest rates, increasing the cost of borrowing. This is because a higher credit score indicates a lower risk to the lender.

SEFCU, like most financial institutions, uses credit scores to assess the risk associated with lending money. A strong credit history demonstrates responsible financial behavior, making you a more attractive borrower. This assessment directly impacts the interest rate you’ll receive.

Credit Score Impact on Specific SEFCU Loan Products

The relationship between credit score and interest rate applies across various SEFCU loan products, including auto loans, personal loans, and mortgages. For instance, a borrower with an excellent credit score (750 or higher) might qualify for a significantly lower interest rate on an auto loan compared to a borrower with a fair credit score (650-699). This difference can amount to hundreds, or even thousands, of dollars in interest paid over the loan term. Similarly, a higher credit score can unlock better terms and lower rates for home equity loans and lines of credit. The exact impact varies depending on the specific loan product, loan amount, and other factors considered during the underwriting process. It’s crucial to check with SEFCU for current rates and eligibility requirements.

Comparison of Credit Score Impact Across Financial Institutions

While the general principle of higher credit scores leading to lower interest rates applies across most financial institutions, the specific impact can vary. Some lenders may have stricter lending criteria or offer a narrower range of interest rates based on credit scores. Others might offer more competitive rates for borrowers with excellent credit. It’s beneficial to compare offers from multiple lenders, including SEFCU, to find the best interest rate for your individual circumstances. Factors beyond credit score, such as debt-to-income ratio and loan-to-value ratio (for mortgages), also play a significant role in determining the final interest rate offered.

Credit Score Ranges and Corresponding Loan Rate Implications

Understanding the general relationship between credit score ranges and interest rates is essential for planning your loan application. The following is a general illustration and should not be considered a definitive guide, as actual rates offered by SEFCU may vary based on several other factors.

The impact of credit score on interest rates is significant, and obtaining a higher credit score before applying for a loan can lead to substantial savings.

| Credit Score Range | Potential Interest Rate Impact (Illustrative Example) |

|---|---|

| Excellent (750+) | Lowest available interest rates; potentially significant discounts |

| Good (700-749) | Favorable interest rates, generally within a competitive range |

| Fair (650-699) | Higher interest rates compared to good or excellent credit; may require a larger down payment or higher fees |

| Poor (Below 650) | Significantly higher interest rates; may face loan denial or limited loan options |

Loan Rate Calculation and Fees

SEFCU’s loan interest rates are not publicly listed as a simple, fixed rate. Instead, they are determined on a case-by-case basis, considering several key factors related to the borrower and the loan itself. Understanding this process allows borrowers to better anticipate their loan costs and make informed financial decisions.

SEFCU uses a complex algorithm to calculate its loan interest rates. This algorithm incorporates various factors, including the applicant’s credit score, the loan amount, the loan term, the type of loan (e.g., auto loan, personal loan, mortgage), and the prevailing market interest rates. A higher credit score generally results in a lower interest rate, while a larger loan amount or a longer loan term may lead to a higher rate. The specific weighting of these factors is proprietary information not publicly disclosed by SEFCU. However, understanding the general principles allows for a better grasp of the rate calculation.

Factors Influencing SEFCU Loan Interest Rates

Several factors significantly influence the interest rate SEFCU applies to a loan. These factors interact in a complex way, meaning a small change in one factor can have a disproportionate effect on the final rate. For example, a slightly lower credit score might result in a noticeably higher interest rate, increasing the overall cost of the loan significantly. Predicting the exact rate without access to SEFCU’s internal algorithm is impossible, but understanding these factors allows for informed planning.

- Credit Score: A higher credit score typically results in a lower interest rate, reflecting the lower perceived risk to the lender.

- Loan Amount: Larger loan amounts might be associated with slightly higher interest rates, potentially due to increased risk.

- Loan Term: Longer loan terms generally result in higher interest rates due to the increased time value of money and the longer period of risk for the lender.

- Loan Type: Different loan types (e.g., auto loans versus personal loans) carry varying levels of risk and may have different base interest rates.

- Prevailing Market Interest Rates: SEFCU’s rates are influenced by broader economic conditions and the prevailing interest rates in the financial markets. Rising market rates generally lead to higher loan rates.

Examples of SEFCU Loan Fees

In addition to the interest rate, various fees are associated with SEFCU loans. These fees can significantly impact the overall cost, and understanding them is crucial for budgeting purposes. The specific fees and their amounts can vary depending on the loan type and the borrower’s circumstances.

- Application Fee: A one-time fee charged for processing the loan application.

- Origination Fee: A fee charged to cover the administrative costs of setting up the loan.

- Late Payment Fee: A penalty fee for missed or late loan payments.

- Prepayment Penalty: A fee charged if the borrower pays off the loan early. This is not always applicable to all SEFCU loans.

Total Loan Cost Comparison, Sefcu loan rates

To illustrate the impact of different interest rates and fees, consider two hypothetical scenarios for a $10,000 personal loan with a 5-year term:

| Scenario | Interest Rate | Origination Fee | Monthly Payment (approx.) | Total Interest Paid (approx.) | Total Loan Cost (approx.) |

|---|---|---|---|---|---|

| Scenario 1 | 6% | $100 | $193 | $1150 | $11,250 |

| Scenario 2 | 8% | $100 | $203 | $1,750 | $11,850 |

Note: These are approximate figures and do not include potential late payment fees. The actual monthly payment and total interest paid will depend on the exact loan terms and SEFCU’s calculation method.

Total Interest Calculation

The total interest paid over the loan term is calculated using an amortization schedule. This schedule details the breakdown of each payment into principal and interest components over the loan’s life. While SEFCU likely uses sophisticated software for this calculation, a simplified formula can provide a general estimate:

Total Interest = (Monthly Payment * Number of Payments) – Loan Amount

For Scenario 1 above: Total Interest ≈ ($193 * 60) – $10,000 = $1150. This is an approximation; the actual amount may vary slightly due to the way interest is compounded. Similar calculations can be performed for other scenarios to illustrate the impact of varying interest rates and fees on the total cost of borrowing.

SEFCU Loan Rate Promotions and Specials

SEFCU, like many financial institutions, periodically offers special promotions and discounts on its loan rates to attract new members and reward existing ones. These promotions can significantly impact the overall cost of borrowing, making it crucial for potential borrowers to understand the details and eligibility requirements. It’s important to note that these promotions are subject to change and may not always be available. Therefore, it’s always recommended to check SEFCU’s official website or contact a representative directly for the most up-to-date information.

SEFCU loan rate promotions typically involve reduced interest rates, waived fees, or other incentives for specific loan types, such as auto loans, home equity loans, or personal loans. The terms and conditions of these promotions vary considerably, encompassing factors such as loan amount, loan term, credit score requirements, and the promotional period. Understanding these details is essential for determining whether a particular promotion aligns with your financial goals and circumstances.

Current SEFCU Loan Rate Promotions

To accurately reflect current SEFCU loan rate promotions, a direct check of SEFCU’s official website is necessary. Since promotional offers change frequently, any information provided here might be outdated. The following is a hypothetical example to illustrate the structure of such promotions. Remember to consult SEFCU’s official channels for the most current offers.

Example of a Hypothetical SEFCU Auto Loan Promotion

Let’s assume SEFCU is currently running a promotion for auto loans offering a reduced interest rate for a limited time.

This hypothetical promotion might offer a 2.99% APR on new auto loans for a 60-month term, for borrowers with a credit score of 700 or higher. The promotion might be valid for applications submitted within a specific timeframe, such as the month of October. Furthermore, there might be limitations on the types of vehicles eligible for the promotion, excluding, for example, motorcycles or RVs. There may also be stipulations about the lender from whom the vehicle is purchased. Additional fees might still apply, such as origination fees or early repayment penalties.

Benefits and Drawbacks of Accepting SEFCU Loan Rate Promotions

The decision of whether to take advantage of a SEFCU loan rate promotion involves weighing the benefits against the potential drawbacks.

A key benefit is, of course, the lower interest rate or reduced fees, resulting in significant savings over the loan term. However, it is crucial to consider the eligibility criteria. If you don’t meet the requirements, you won’t qualify for the promotion, and you may end up with a higher interest rate than initially anticipated. Additionally, the promotional period is limited, so you must ensure you can meet the loan terms within that time frame. Finally, carefully examine all terms and conditions; hidden fees or penalties could offset some of the savings.

Key Features of Hypothetical SEFCU Loan Promotions

The following bulleted list summarizes the key features of our hypothetical SEFCU auto loan promotion. Remember that these features are illustrative and should not be considered a reflection of current offers. Always consult SEFCU for the most accurate information.

- Reduced APR: 2.99%

- Loan Term: 60 months

- Credit Score Requirement: 700 or higher

- Promotional Period: October (hypothetical)

- Vehicle Type Restrictions: May exclude certain vehicle types

- Potential Fees: Origination fees may apply

Last Point

Securing a loan can feel overwhelming, but understanding the intricacies of SEFCU loan rates empowers you to make smart financial choices. This guide has equipped you with the knowledge to compare rates, assess the impact of your credit score, and navigate any special offers. Remember to carefully review all terms and conditions before committing to a loan, and don’t hesitate to contact SEFCU directly with any questions. Armed with this information, you can confidently approach the loan application process and find the best financial solution for your needs.

Question Bank: Sefcu Loan Rates

What happens if I miss a SEFCU loan payment?

Missing a payment can result in late fees and negatively impact your credit score. Contact SEFCU immediately if you anticipate difficulty making a payment to explore options like a payment plan.

Can I refinance my existing loan with SEFCU?

SEFCU may offer refinancing options; check their website or contact them directly to inquire about eligibility and current rates.

How long does it take to get approved for a SEFCU loan?

Approval times vary depending on the loan type and the completeness of your application. Generally, expect the process to take several business days.

Does SEFCU offer pre-approval for loans?

Yes, many credit unions offer pre-approval, which allows you to see what rates you qualify for before formally applying. Check SEFCU’s website for details.