Tribal loans no teletrack direct lender: Navigating this financial landscape requires careful consideration. These loans, offered by tribal lenders, bypass traditional credit checks, potentially making them accessible to those with poor credit. However, this convenience comes with significant risks. Understanding the legal framework, interest rates, and potential pitfalls is crucial before considering this type of loan. This guide provides a comprehensive overview, exploring the benefits, drawbacks, and alternatives to help you make an informed decision.

We’ll delve into the specifics of “no teletrack” lending, examining how lenders verify borrower information without relying on credit bureaus. We’ll also compare the processes and costs of borrowing from direct tribal lenders versus third-party lenders, highlighting potential red flags to watch out for. Finally, we’ll explore alternative financing options and strategies for managing debt effectively, empowering you to make responsible financial choices.

Understanding Tribal Loans

Tribal loans are short-term, high-interest loans offered by lenders affiliated with Native American tribes. These loans often target individuals with poor credit history who may have difficulty obtaining financing through traditional channels. Understanding their unique characteristics and the legal landscape surrounding them is crucial for potential borrowers.

Tribal loans operate under a complex legal framework. Lenders assert that their tribal affiliation shields them from state usury laws, which typically cap interest rates. This assertion, however, is frequently contested, with many states actively challenging the jurisdictional claims of tribal lenders. The legal battles surrounding tribal lending are ongoing and highly complex, impacting the availability and terms of these loans.

Characteristics of Tribal Loans

Tribal loans share some similarities with payday loans, but key distinctions exist. Both are typically small, short-term loans designed to bridge a financial gap until the borrower’s next payday. However, tribal loans often carry even higher interest rates and fees than payday loans, and their repayment terms can be equally stringent. The lack of clear regulatory oversight in some jurisdictions contributes to the higher costs and risks associated with tribal loans. Furthermore, the collection practices employed by some tribal lenders have drawn criticism.

Legal Framework of Tribal Lending

The legal standing of tribal lending is a subject of ongoing debate. The core argument hinges on the principle of tribal sovereignty—the inherent right of Native American tribes to govern themselves within their reservations. Lenders argue that this sovereignty allows them to operate outside of state regulations, including usury laws. Conversely, many states argue that these loans affect their citizens and thus fall under their jurisdiction. Court cases and legislative actions continue to shape the legal landscape, leading to uncertainty for both lenders and borrowers.

Comparison with Traditional Payday Loans

While both tribal loans and traditional payday loans are short-term, high-cost loans, several key differences exist. Payday loans are generally more regulated at the state level, leading to greater consumer protections in many jurisdictions. Tribal loans, due to their claimed exemption from state laws, often lack such protections. This lack of regulation can result in higher interest rates, more aggressive collection practices, and fewer options for borrowers facing difficulty in repayment. The lack of clear, consistent regulation across the nation makes comparison difficult, but the general trend indicates higher costs and risks with tribal loans.

Situations Where a Tribal Loan Might Be Considered

A borrower might consider a tribal loan only as a last resort, after exhausting all other options. This could be a situation where an individual faces an immediate, unavoidable expense (e.g., emergency car repair, unexpected medical bill) and has exhausted savings and credit options. It is crucial to understand that this is a high-risk financial decision, and the high interest rates and fees can quickly lead to a debt cycle that is difficult to escape. Exploring alternative solutions, such as negotiating with creditors, seeking financial counseling, or applying for a small loan from a credit union or bank, should always be prioritized before considering a tribal loan. Borrowers should carefully weigh the potential risks and benefits before proceeding.

No Teletrack Aspect

Tribal lenders offering “no teletrack” loans advertise a streamlined application process, often appealing to borrowers with damaged credit histories. The absence of Teletrack, a credit reporting agency, signifies that these lenders don’t access this specific database to assess creditworthiness. This approach can lead to faster approvals, but it also carries significant implications for both borrowers and lenders.

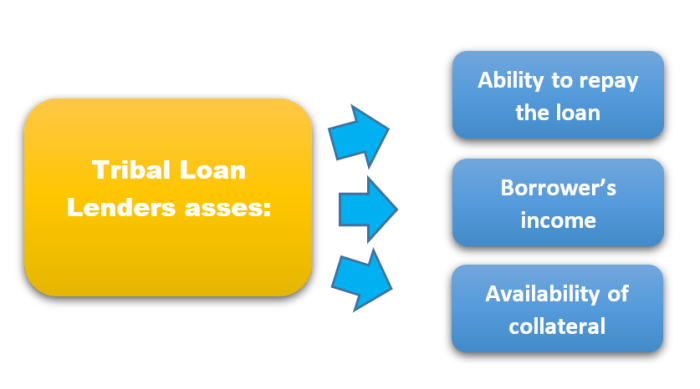

The core difference lies in how lenders verify borrower information. Traditional lenders rely heavily on Teletrack and other credit bureaus (like Equifax, Experian, and TransUnion) to build a comprehensive credit profile. This includes reviewing past payment history, outstanding debts, and credit utilization. In contrast, no-teletrack lenders employ alternative methods, such as verifying income through pay stubs or bank statements, and assessing debt-to-income ratios. They may also use proprietary scoring models or focus heavily on the applicant’s ability to repay the loan based on their current financial situation.

Alternative Verification Methods Used by No-Teletrack Lenders

No-teletrack lenders utilize various methods to assess the creditworthiness of applicants. These often include rigorous income verification, requiring detailed pay stubs, bank statements, and employment verification. They may also request proof of address and other identifying documents to mitigate the risk of fraud. Some lenders may incorporate alternative credit scoring systems, which analyze data points beyond traditional credit reports, such as rent payment history or utility bill payments. This multi-faceted approach allows them to make lending decisions without relying solely on Teletrack data.

Credit Reporting Implications: Teletrack vs. Non-Teletrack Lenders

The primary difference lies in how the loan application impacts a borrower’s credit report. Loans processed through Teletrack lenders are typically reported to the major credit bureaus. This means on-time payments improve credit scores, while missed payments negatively affect them. Conversely, loans from non-teletrack lenders generally do not get reported to these bureaus. While this can seem beneficial for those with poor credit, it also means that responsible repayment won’t boost their credit score. Consequently, consistently paying back a no-teletrack loan won’t directly improve credit standing in the traditional sense. Conversely, defaulting on a no-teletrack loan won’t appear on a credit report, but it will likely damage the borrower’s relationship with the lender, potentially leading to further difficulties obtaining future loans.

Potential Risks Associated with Non-Teletrack Lenders

The lack of traditional credit checks opens the door to potential risks. Borrowers may encounter higher interest rates due to the increased perceived risk for lenders. Furthermore, some non-teletrack lenders may engage in predatory lending practices, offering loans with exorbitant fees or unfavorable terms. Thorough research and comparison of lenders are crucial before applying for a no-teletrack loan. It’s also essential to carefully read all loan documents to fully understand the terms and conditions before signing any agreement. Borrowers should be wary of lenders who pressure them into accepting a loan without providing sufficient information or time to review the details. The lack of credit reporting also means that defaulting on a loan won’t appear on a credit report, but it could still negatively impact the borrower’s financial future through collection agencies or legal actions.

Direct Lender Focus

Tribal loans offered by direct lenders present a unique lending landscape, differing significantly from those facilitated through third-party brokers. Understanding the nuances of dealing directly with a tribal lender is crucial for borrowers to make informed decisions and avoid potential pitfalls. This section will explore the advantages and disadvantages of this approach, comparing it to using a third-party lender and highlighting key aspects such as fees, interest rates, and potential red flags.

Direct lenders, in the context of tribal loans, are the lending institutions themselves, eliminating the intermediary. This contrasts with third-party lenders, who act as brokers, connecting borrowers with various lenders. This direct relationship can offer certain benefits, but also carries specific risks.

Benefits and Drawbacks of Borrowing from a Direct Lender

Borrowing directly from a tribal lender can potentially streamline the application process, as there’s no need for a third party to review and forward your application. It can also potentially lead to faster funding, though this isn’t always guaranteed. However, drawbacks include a potentially limited range of loan options compared to a broker who can access multiple lenders. Direct lenders may also have stricter lending criteria, potentially leading to higher rejection rates. Furthermore, a lack of comparison shopping options could result in higher interest rates or less favorable terms than those available through a broker who can offer various loan products.

Comparison of Loan Processes: Direct Lender vs. Third-Party Lender

Obtaining a loan from a direct tribal lender typically involves submitting an application directly to the lender’s website or through their physical location, if applicable. This application process usually requires providing personal and financial information. The lender then reviews the application and makes a decision. Contrastingly, using a third-party lender involves submitting one application that’s then forwarded to multiple lenders. This approach offers broader access to loan options but might involve a longer processing time due to the additional steps involved. The third-party lender might also collect fees for their services, which adds to the overall cost of borrowing.

Typical Fees and Interest Rates Associated with Direct Tribal Lenders, Tribal loans no teletrack direct lender

Interest rates and fees for tribal loans from direct lenders can vary significantly based on factors such as creditworthiness, loan amount, and repayment terms. These rates are often higher than those offered by traditional banks or credit unions, reflecting the higher risk associated with this type of lending. Expect fees such as origination fees, late payment fees, and potentially prepayment penalties. It’s crucial to thoroughly review the loan agreement to understand all associated costs before accepting the loan. For example, a $500 loan might have a 200% APR, resulting in significantly higher repayment amounts. Always compare APRs across different lenders before committing.

Potential Red Flags When Dealing with Direct Tribal Lenders

Several red flags should raise concerns when dealing with direct tribal lenders. These include extremely high interest rates and fees that significantly exceed those offered by traditional lenders, vague or unclear loan terms, aggressive or high-pressure sales tactics, and requests for upfront fees before loan approval. A lack of transparency regarding the lender’s licensing and regulatory compliance should also be a significant cause for concern. If a lender makes promises that seem too good to be true, it likely is. For instance, claims of guaranteed approval regardless of credit history or the inability to provide clear information about licensing should prompt immediate caution. Always verify the lender’s legitimacy through independent research before committing to a loan.

Loan Repayment and Default

Tribal loans, like other short-term loans, typically involve a repayment schedule that Artikels the amount and frequency of payments. Understanding this schedule and adhering to it is crucial to avoid the serious consequences of default. This section details repayment options, the repercussions of default, and strategies for managing tribal loan debt effectively.

Repayment options for tribal loans generally mirror those of other short-term loans. Borrowers usually make fixed payments over a predetermined period, often weekly or bi-weekly, directly to the lender. Some lenders may offer options to adjust payment amounts or extend the repayment term, although this often comes with additional fees. It’s vital to review the loan agreement thoroughly to understand the specific repayment terms and any potential penalties for late or missed payments. Failure to fully understand the terms can lead to unexpected costs and financial difficulty.

Repayment Options

Typical repayment methods include automated bank withdrawals, online payments, and mailed checks. The specific methods accepted will vary depending on the lender. Borrowers should confirm their preferred payment method with the lender to ensure timely and accurate payments. Choosing a method that aligns with personal financial management practices is crucial for avoiding late payments.

Consequences of Default

Defaulting on a tribal loan can have severe financial repercussions. These consequences can range from additional fees and penalties to damage to credit scores, debt collection actions, and even legal proceedings. Late payment fees can significantly increase the total amount owed, making it even more difficult to repay the loan. Repeated defaults can severely impact a borrower’s creditworthiness, making it harder to obtain credit in the future. Furthermore, aggressive debt collection practices, including phone calls, letters, and potential legal action, can create significant stress and financial hardship.

Disputing Charges or Errors

If a borrower believes there are errors or discrepancies in their loan statement, they should immediately contact the lender to initiate a dispute. Documentation of all communication, including dates, times, and the content of conversations, is crucial. Keeping a detailed record of payments made and any discrepancies noted helps build a strong case for a dispute. If the dispute remains unresolved, the borrower may need to seek assistance from consumer protection agencies or legal counsel.

Strategies for Managing Tribal Loan Debt

Effective management of tribal loan debt requires proactive planning and responsible financial behavior. Creating a realistic budget that accounts for all income and expenses is a crucial first step. This allows borrowers to identify areas where they can reduce spending and allocate funds towards loan repayment. Exploring options such as debt consolidation or seeking financial counseling can also help manage and potentially reduce the overall debt burden. For example, a borrower struggling with multiple high-interest loans might benefit from consolidating them into a single loan with a lower interest rate. Financial counseling provides personalized guidance on budgeting, debt management, and financial planning.

Consumer Protection and Risks

Tribal loans, while offering a potentially convenient borrowing option for those with less-than-perfect credit, present significant risks to consumers. Understanding these risks and the applicable consumer protection laws is crucial before considering such a loan. The high-interest rates and often opaque terms can lead to a debt trap if not carefully managed.

Potential risks associated with tribal loans stem primarily from the complex regulatory landscape and the often aggressive lending practices employed by some lenders. These risks are amplified by the lack of consistent federal oversight and the challenges in enforcing state consumer protection laws against tribal lenders.

High Interest Rates and Fees

Tribal lenders frequently charge significantly higher interest rates and fees compared to traditional lenders. These elevated costs can quickly escalate the total loan amount, making repayment difficult and potentially leading to a cycle of debt. For example, a loan with a 200% APR would quickly accumulate substantial interest, dwarfing the initial principal amount. This can result in borrowers paying back far more than they initially borrowed.

Aggressive Collection Practices

Some tribal lenders have been accused of employing aggressive debt collection tactics, including harassing phone calls, threats, and public shaming. These tactics can cause significant emotional distress and financial hardship for borrowers. Such practices are often in violation of state and federal fair debt collection laws, but enforcement can be challenging due to the jurisdictional complexities involved in tribal lending.

Lack of Clear Loan Terms

The terms and conditions of tribal loans are sometimes unclear or intentionally obfuscated, making it difficult for borrowers to fully understand the cost of borrowing. Hidden fees and complex repayment schedules can lead to unexpected expenses and financial difficulties. A borrower might agree to a loan believing the terms are manageable, only to discover later that the true cost is far greater than anticipated.

Limited Consumer Protection

While some consumer protection laws apply to tribal lending, enforcement can be difficult due to the sovereign immunity of tribal nations. This means that state and federal courts may have limited jurisdiction over tribal lenders, making it challenging for borrowers to seek redress for unfair or deceptive lending practices. This jurisdictional ambiguity leaves borrowers with fewer legal avenues for recourse compared to loans from traditional lenders.

Resources for Borrowers Struggling with Tribal Loan Debt

Consumers struggling with tribal loan debt can seek assistance from several resources. These include non-profit credit counseling agencies that can offer guidance on debt management and negotiation with lenders. State attorney general’s offices may also provide assistance with complaints against lenders engaged in unfair or deceptive practices. Finally, the Consumer Financial Protection Bureau (CFPB) offers resources and information on consumer rights and protections related to all types of loans, including those from tribal lenders. Utilizing these resources can help borrowers navigate the complexities of debt and potentially find solutions to their financial challenges.

Alternatives to Tribal Loans: Tribal Loans No Teletrack Direct Lender

Tribal loans, while offering quick access to funds, often come with high interest rates and potential risks. Exploring alternative financing options is crucial for borrowers seeking responsible and affordable solutions. Understanding the costs and benefits of each alternative can empower consumers to make informed financial decisions.

Comparison of Alternative Financing Options

Several alternatives to tribal loans exist, each with its own set of advantages and disadvantages. Careful consideration of individual financial circumstances is key to selecting the most suitable option. The following table compares common alternatives, focusing on accessibility, cost, and repayment terms.

| Loan Type | Pros | Cons | Suitability |

|---|---|---|---|

| Credit Union Loans | Lower interest rates than many other options, often member benefits, potential for personalized service. | Membership requirements, may require good credit history. | Suitable for borrowers with good or fair credit who meet membership requirements. |

| Bank Loans | Potentially lower interest rates than payday loans, various loan types available (personal, secured). | Stricter credit requirements, longer application process. | Suitable for borrowers with established credit history and a need for larger loan amounts. |

| Payday Alternative Loans (PALs) from Credit Unions | Smaller loan amounts with longer repayment terms than traditional payday loans, lower interest rates. | Credit union membership required, loan amounts may be limited. | Suitable for borrowers who need a short-term loan and meet credit union membership requirements. |

| Personal Loans from Online Lenders | Quick application and approval process, potentially flexible repayment terms. | Interest rates can vary widely, potential for high fees, less personal service. | Suitable for borrowers with good or fair credit who need quick access to funds and can compare offers. |

| Peer-to-Peer (P2P) Lending | Potential for lower interest rates than traditional lenders, wider range of credit scores accepted. | Higher risk for lenders, potentially longer application process, repayment terms may vary significantly. | Suitable for borrowers with fair to good credit willing to navigate a potentially more complex application process. |

Assessing Suitability Based on Individual Circumstances

Choosing the right loan depends heavily on individual financial situations. Factors to consider include credit score, income stability, debt-to-income ratio, and the loan amount needed. For example, a borrower with a high credit score and stable income might qualify for a bank loan with a favorable interest rate, while someone with a lower credit score might find a credit union’s PAL more accessible. Careful budgeting and a clear understanding of repayment terms are essential regardless of the chosen loan type. Borrowers should always compare offers from multiple lenders before committing to a loan to secure the best possible terms.

Closing Summary

Securing a tribal loan no teletrack direct lender requires a thorough understanding of the associated risks and benefits. While the convenience of bypassing traditional credit checks is alluring, high interest rates and potential predatory lending practices necessitate careful evaluation. By weighing the pros and cons, exploring alternative financing options, and prioritizing responsible borrowing habits, you can navigate this complex financial landscape effectively and make the best decision for your unique circumstances. Remember, thorough research and careful planning are paramount.

Clarifying Questions

What are the legal implications of tribal loans?

The legal landscape surrounding tribal lending is complex and varies by state. Jurisdictional issues often arise due to the sovereign immunity of tribal nations. It’s crucial to understand the specific laws governing tribal lending in your state before proceeding.

How are interest rates determined for tribal loans?

Interest rates on tribal loans are influenced by several factors, including the borrower’s creditworthiness (even without a traditional credit check), the loan amount, and the repayment term. These rates can be significantly higher than those offered by traditional lenders.

What happens if I default on a tribal loan?

Defaulting on a tribal loan can result in significant financial consequences, including debt collection actions, damage to your credit score (even without teletrack), and potential legal repercussions. Understanding the repayment terms and adhering to them is crucial.

Are there consumer protection agencies that can help with tribal loan issues?

While consumer protection laws may apply, their effectiveness in addressing issues with tribal lenders can be limited due to jurisdictional complexities. State attorneys general and consumer protection agencies can offer guidance and assistance, but success is not guaranteed.