NBT solar loan options offer a pathway to sustainable energy, but understanding the intricacies is key. This comprehensive guide navigates the process of securing an NBT solar loan, from eligibility requirements and interest rates to repayment plans and potential government incentives. We’ll explore the advantages and disadvantages, compare it to alternative financing methods, and share insights from real customer experiences to help you make an informed decision.

We’ll delve into the specifics of NBT’s loan features, providing a step-by-step application guide and comparing their offerings to other financial solutions. Understanding repayment schedules, potential late payment consequences, and the total cost of ownership are crucial aspects we will cover in detail. We’ll also examine how government incentives and tax benefits can influence your loan eligibility and overall cost.

Understanding NBT Solar Loans

NBT Bank offers solar loans designed to help homeowners finance the installation of solar energy systems. These loans provide a streamlined financing option, allowing individuals to invest in renewable energy and potentially reduce their long-term energy costs. Understanding the features, eligibility requirements, and associated costs is crucial before applying.

Typical Features of NBT Solar Loans

NBT solar loans typically offer competitive interest rates and flexible repayment terms tailored to individual financial situations. Loan amounts vary depending on the project’s cost and the borrower’s creditworthiness. Many programs also include options for fixed interest rates, protecting borrowers from fluctuating interest rate environments. Additional features might include loan pre-approval processes, enabling prospective borrowers to know their financing options before finalizing a solar installation contract. Finally, some programs may integrate with approved solar installers, providing a seamless transition from financing to installation.

Eligibility Criteria for NBT Solar Loans

Eligibility for an NBT solar loan typically involves meeting specific financial criteria. These often include a minimum credit score, a stable income demonstrating consistent repayment ability, and sufficient equity in the property where the solar system will be installed. NBT Bank will assess the borrower’s debt-to-income ratio (DTI) to ensure the loan fits within their overall financial capacity. Providing accurate and complete documentation, such as tax returns, pay stubs, and proof of homeownership, is vital throughout the application process. Specific requirements might vary based on the loan program and the applicant’s circumstances. Pre-qualification can help determine eligibility before a formal application.

Comparison of NBT Solar Loan Interest Rates

NBT solar loan interest rates are competitive within the market, though the exact rate will depend on factors such as the borrower’s credit score, loan amount, and repayment term. Direct comparison to other financing options, such as home equity loans or personal loans, requires considering the total cost of borrowing, including interest rates, fees, and repayment periods. For instance, a home equity loan might offer a lower interest rate but require higher equity, while a personal loan might have higher interest rates and shorter repayment terms. It’s essential to compare multiple financing options from different lenders to find the most suitable choice for individual financial needs and circumstances. Always thoroughly review loan terms and conditions before committing.

Applying for an NBT Solar Loan: A Step-by-Step Guide

The application process for an NBT solar loan typically begins with pre-qualification to determine eligibility and obtain an estimated interest rate. Next, borrowers will need to gather the necessary documentation, including proof of income, credit report, and property details. A formal application is then submitted to NBT Bank, which will review the provided information and assess the applicant’s creditworthiness. Upon approval, the loan terms are finalized, including the interest rate, repayment schedule, and loan amount. Finally, the funds are disbursed, usually directly to the solar installer after the system’s installation is complete. Throughout this process, clear communication with NBT Bank is crucial to address any questions or concerns.

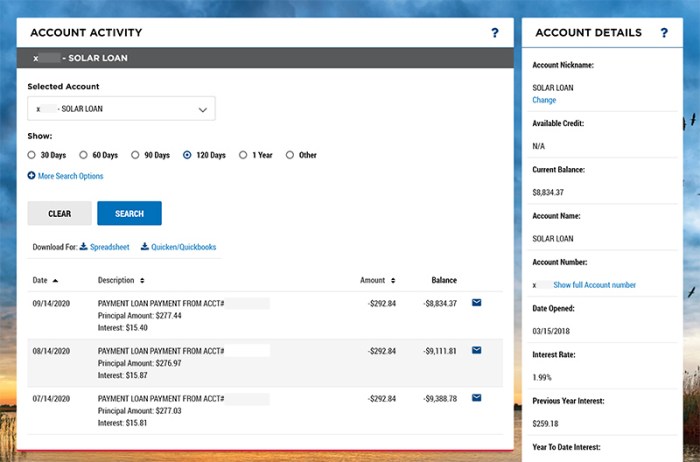

NBT Solar Loan Repayment Options

Choosing the right repayment schedule for your NBT solar loan is crucial for managing your finances effectively. Understanding the various options available, their associated costs, and the consequences of missed payments will empower you to make informed decisions. This section details the repayment structures offered by NBT and highlights important considerations.

Repayment Schedules Available

NBT Solar Loans typically offer a range of repayment schedules tailored to individual financial situations. These often include fixed-term loans with monthly installments spread over a predetermined period (e.g., 5, 10, or 15 years). The length of the loan significantly impacts the monthly payment amount and the total interest paid over the loan’s lifetime. Shorter-term loans result in higher monthly payments but lower overall interest, while longer-term loans have lower monthly payments but higher overall interest costs. Some lenders may also offer flexible repayment options, allowing borrowers to adjust their payment amounts or frequency under specific circumstances, though this is not always standard practice. It’s essential to discuss available options with your loan officer.

Examples of Repayment Plans and Associated Costs

Let’s consider two hypothetical examples to illustrate the differences between repayment plans. Assume a $20,000 solar loan with a 5% annual interest rate.

Example 1: 5-Year Loan

A 5-year loan might have a monthly payment of approximately $377. The total interest paid over the life of the loan would be significantly less than a longer-term loan. However, the monthly payment is substantially higher.

Example 2: 15-Year Loan

A 15-year loan for the same amount might have a monthly payment of approximately $160. The monthly payment is considerably lower, making it more manageable for some borrowers. However, the total interest paid over the 15 years will be substantially greater than the 5-year loan.

These are illustrative examples, and the actual figures will vary depending on the specific loan terms, interest rates, and any applicable fees. Always obtain a detailed loan amortization schedule from NBT to understand the exact breakdown of payments and interest.

Consequences of Late or Missed Payments

Late or missed payments on your NBT solar loan can have serious financial consequences. These may include:

* Late payment fees: NBT will likely charge late fees for each missed or late payment. These fees can add up significantly over time.

* Negative impact on credit score: Late payments are reported to credit bureaus, negatively impacting your credit score. This can make it more difficult to obtain credit in the future, such as mortgages or auto loans.

* Loan default: Repeated or prolonged failure to make payments can lead to loan default. This could result in the lender taking legal action to recover the outstanding debt, potentially including repossession of assets (though this is less likely with a solar loan secured on the property itself).

* Increased interest rates: Consistent late payments might cause NBT to increase your interest rate, further increasing the total cost of your loan.

Comparison of Repayment Options

| Loan Term (Years) | Approximate Monthly Payment | Total Interest Paid (Estimate) | Advantages |

|---|---|---|---|

| 5 | $377 | $4,620 | Lower total interest, faster payoff |

| 10 | $210 | $8,200 | Lower monthly payment |

| 15 | $160 | $12,000 | Lowest monthly payment |

Benefits and Drawbacks of NBT Solar Loans

Choosing to finance your solar energy system through a loan, specifically an NBT solar loan, presents a complex equation of advantages and disadvantages. Understanding these aspects is crucial for making an informed decision that aligns with your financial goals and long-term energy strategy. A thorough assessment will allow you to weigh the potential benefits against the associated costs and limitations.

This section will analyze the key advantages and disadvantages of using an NBT solar loan to fund your solar energy project, providing a comparative analysis of total cost of ownership with and without financing. This analysis will empower you to make a well-informed decision.

Advantages of NBT Solar Loans

Securing a solar loan through NBT can offer several compelling advantages. These benefits primarily center around affordability, accessibility, and the potential for long-term cost savings. The accessibility of financing can make solar energy a viable option for homeowners who might otherwise be unable to afford the upfront costs of installation.

The lower monthly payments offered by a loan can be significantly less than the monthly electricity bill savings generated by the solar system. This means that, in many cases, the loan payment is offset by reduced energy costs, resulting in a net positive financial outcome. Moreover, NBT may offer various loan terms and interest rates tailored to individual circumstances, ensuring flexibility and potentially lower overall costs. The potential for tax credits and other government incentives can further reduce the effective cost of the loan and the overall solar investment.

Disadvantages of NBT Solar Loans

While NBT solar loans provide access to clean energy, it’s essential to acknowledge potential drawbacks. The primary disadvantage is the accumulation of interest over the loan’s lifespan, leading to a higher total cost of ownership compared to paying cash upfront. This increased cost should be carefully weighed against the long-term savings from reduced energy bills.

Furthermore, the loan application process may involve credit checks and other requirements that could pose challenges for some applicants. The terms and conditions of the loan, including interest rates and repayment schedules, must be thoroughly understood before signing the agreement. Changes in interest rates during the loan term could also impact the total cost. Finally, the value of the solar system might depreciate over time, potentially leading to a situation where the loan amount exceeds the system’s remaining worth.

Total Cost of Ownership Comparison

A comprehensive comparison of total cost of ownership (TCO) with and without an NBT solar loan is vital. The TCO without a loan represents the upfront cost of the solar system installation. The TCO with a loan includes the total loan repayment amount (principal plus interest) over the loan’s term.

For example, let’s assume a $20,000 solar system. Without a loan, the upfront cost is $20,000. With a 10-year NBT loan at a 5% interest rate, the total repayment could be significantly higher, potentially exceeding $25,000, depending on the specific loan terms. However, this increased cost must be weighed against the monthly savings from reduced energy bills over the same period. A detailed financial analysis, considering energy cost savings, potential tax credits, and loan interest, is essential to determine the most cost-effective option.

Pros and Cons Summary

To summarize the key advantages and disadvantages, consider the following:

- Pros: Increased affordability, accessibility to solar energy for a wider range of homeowners, potential for significant long-term cost savings due to reduced energy bills, flexible loan terms and potentially lower interest rates, eligibility for government incentives and tax credits.

- Cons: Accumulation of interest leading to higher total cost compared to cash purchase, potential credit check requirements, need for thorough understanding of loan terms and conditions, risk of interest rate fluctuations, possibility of loan amount exceeding system’s depreciated value.

NBT Solar Loan and Government Incentives

Navigating the landscape of solar energy financing can be significantly impacted by various government incentives. Understanding how these incentives interact with NBT solar loans is crucial for maximizing savings and streamlining the loan application process. This section details the potential influence of government programs on loan eligibility and the associated tax benefits.

Government Incentives and Loan Eligibility

Government incentives, such as tax credits or rebates, can directly influence your eligibility for an NBT solar loan. Lenders often consider the increased financial viability resulting from these incentives when assessing loan applications. A larger tax credit, for instance, might reduce the overall loan amount needed, thus improving your creditworthiness and potentially leading to a lower interest rate or more favorable loan terms. Conversely, the absence of such incentives might necessitate a larger loan amount, potentially leading to stricter eligibility requirements. The interplay between the incentive and the loan application is dynamic and specific to each individual’s financial situation and the applicable government programs.

Tax Benefits Associated with NBT Solar Loans

The installation of solar panels often qualifies for significant federal and state tax benefits. The most common is the federal Investment Tax Credit (ITC), which provides a percentage credit on the cost of solar equipment and installation. This credit directly reduces your tax liability, effectively lowering the net cost of your solar system and consequently, your loan repayments. Additionally, some states offer their own tax incentives, such as sales tax exemptions or property tax reductions, which further enhance the financial attractiveness of solar energy investment and can affect the amount you need to borrow. For example, a homeowner might receive a 30% federal ITC and a 10% state rebate, substantially reducing the initial investment and the loan’s burden.

Examples of Government Program Interaction with NBT Loans, Nbt solar loan

Consider a scenario where a homeowner secures a $20,000 NBT solar loan. If they are eligible for a 26% federal ITC, this translates to a $5,200 tax credit. This credit reduces their loan principal to $14,800, significantly lowering their monthly payments and the overall interest paid over the loan’s lifespan. Further, if their state offers a $1,000 rebate, the effective loan amount decreases even further to $13,800. This illustrates how government programs can substantially alter the financial equation, making solar energy more accessible and affordable. Another example could involve a situation where a state offers a “Property Assessed Clean Energy” (PACE) program, allowing homeowners to finance renewable energy improvements through a special assessment on their property taxes. This could be used in conjunction with an NBT solar loan, potentially reducing the upfront cost or allowing for a larger solar system installation.

Available Incentives: A Structured Overview

Understanding the availability and specifics of incentives requires diligent research based on your location and the specifics of the NBT loan. Below is a sample structure to guide your research. Remember that these incentives are subject to change and should be verified with the relevant authorities.

| Incentive Type | Federal Level | State Level | Local Level |

|---|---|---|---|

| Investment Tax Credit (ITC) | [Insert current ITC percentage and details. Link to IRS website for verification] | [Insert state-specific ITC or equivalent. Link to state’s energy office website for verification] | [Insert local incentives if any. Link to relevant local government website] |

| Rebates | [Insert details of any federal rebates] | [Insert details of any state rebates] | [Insert details of any local rebates] |

| Tax Exemptions | [Insert details of any federal tax exemptions] | [Insert details of any state tax exemptions] | [Insert details of any local tax exemptions] |

| PACE Financing | [Information on federal programs related to PACE] | [State-specific information on PACE programs] | [Local program details for PACE] |

Customer Experiences with NBT Solar Loans

NBT Solar Loans has garnered a diverse range of customer experiences, reflecting the individual circumstances and expectations of borrowers. Analyzing these experiences provides valuable insights into the loan process, its effectiveness, and areas for potential improvement. This section presents anonymized case studies showcasing both successful loan applications and challenges faced by some borrowers, ultimately aiming to illustrate overall customer satisfaction levels.

Successful Loan Applications

Several borrowers have reported positive experiences with the NBT Solar Loan application process. For instance, a homeowner in rural Vermont, seeking to install a 5kW solar panel system, found the application straightforward and the loan approval relatively quick. The streamlined online application and clear communication from NBT representatives contributed to a positive experience. Another example involves a small business owner in New Hampshire who successfully leveraged an NBT Solar Loan to finance a larger, 10kW system, significantly reducing their energy costs and boosting their environmental credentials. Their experience highlighted the flexibility of the loan program to accommodate diverse needs. These successful applications underscore the accessibility and efficiency of the NBT Solar Loan program for qualified applicants.

Challenges Faced by Borrowers and Their Resolutions

While many borrowers have had positive experiences, some challenges have emerged. One borrower reported initial difficulty navigating the online application portal. However, after contacting NBT customer support, the issue was quickly resolved with clear, step-by-step guidance. Another borrower experienced a slight delay in loan disbursement due to unforeseen circumstances related to property documentation. NBT worked proactively with the borrower to expedite the process, ensuring minimal disruption to the solar installation timeline. These instances highlight the importance of clear communication and responsive customer service in addressing potential challenges.

Customer Satisfaction Summary

To provide a comprehensive overview of customer feedback, the following table summarizes positive and negative experiences with NBT Solar Loans.

| Positive Feedback | Negative Feedback |

|---|---|

| Easy online application process | Initial difficulty navigating the online portal (resolved with customer support) |

| Quick loan approval | Slight delays in loan disbursement (due to property documentation issues, resolved with proactive communication) |

| Excellent customer service | Limited information available on specific loan terms in some cases |

| Competitive interest rates | Some borrowers experienced a longer-than-expected wait for initial loan application processing |

Alternatives to NBT Solar Loans

Choosing the right financing method for your solar panel installation is crucial, impacting both upfront costs and long-term expenses. While NBT solar loans offer one avenue, several alternatives exist, each with its own set of advantages and disadvantages. Understanding these options allows for a more informed decision based on individual financial situations and long-term goals.

Comparison of NBT Solar Loans with Other Solar Financing Options

NBT solar loans typically involve a fixed interest rate and a set repayment schedule over a specific term, often 10-25 years. Other financing options include cash purchases, home equity loans, and solar leases or Power Purchase Agreements (PPAs). Cash purchases offer the lowest long-term cost but require a significant upfront investment. Home equity loans utilize your home’s equity as collateral, potentially offering lower interest rates than personal loans but increasing your home loan debt. Solar leases and PPAs involve monthly payments to a third-party provider for the use of the solar system, with no ownership transfer. A visual comparison would show a bar graph with the y-axis representing total cost over 20 years and the x-axis representing the financing method (Cash, NBT Loan, Home Equity Loan, Lease/PPA). The cash purchase bar would be the shortest, followed by the home equity loan, then the NBT loan, and finally, the lease/PPA bar would be the longest, reflecting the cumulative cost over time.

Leasing Versus Purchasing Solar Panels

Leasing solar panels (through a PPA) eliminates the upfront cost but results in ongoing monthly payments. This payment structure may be preferable for those with limited upfront capital but can lead to significantly higher overall costs compared to purchasing. Purchasing, on the other hand, requires a larger initial investment but provides ownership of the system and potential long-term cost savings through avoided electricity bills and potential tax credits. A direct comparison might illustrate this using a hypothetical scenario: A $20,000 solar panel system with a 20-year lifespan. A lease might cost $100/month, totaling $24,000 over 20 years. A loan with a 5% interest rate over 15 years might result in a total repayment of $25,000, including interest. While the loan requires an upfront down payment (potentially offset by tax credits), the overall cost is still lower than leasing. The cash purchase, assuming no financing, would cost $20,000.

Long-Term Cost Differences Across Financing Methods

The long-term cost of solar panel ownership significantly varies depending on the financing method. Cash purchases represent the lowest total cost over the system’s lifespan. Loans, including NBT solar loans, involve interest payments, increasing the total cost compared to a cash purchase but still potentially less than leasing. Leases and PPAs often have the highest long-term costs due to the extended monthly payments, effectively making them a long-term rental agreement. For example, a 20-year lease on a $25,000 system might cost $35,000 in total, significantly more than the initial system cost. A 15-year loan at 6% interest on the same system might cost approximately $32,000, showing a considerable difference compared to leasing but higher than a cash purchase.

Final Thoughts

Securing financing for solar energy can feel daunting, but with a clear understanding of NBT solar loan options and alternatives, you can make a confident choice. By carefully weighing the benefits, drawbacks, and potential government incentives, you can determine if an NBT solar loan aligns with your financial goals and commitment to renewable energy. Remember to thoroughly research and compare options before making a final decision.

FAQ Compilation

What credit score is typically required for an NBT solar loan?

While specific requirements vary, a good to excellent credit score (generally above 670) is usually necessary for approval.

Can I refinance my existing NBT solar loan?

NBT may offer refinancing options; contact them directly to explore possibilities based on your current loan terms and financial situation.

What happens if my solar panel system malfunctions after receiving an NBT loan?

Warranty coverage and potential repair costs should be clarified during the loan application process. Your loan agreement should Artikel procedures for handling such situations.

Are there prepayment penalties with an NBT solar loan?

Check your loan agreement for details on prepayment penalties. Some loans may have penalties for paying off the loan early, while others may not.