GECU auto loans provide a compelling option for car financing, offering a range of loan types and competitive interest rates. This comprehensive guide delves into the specifics of GECU’s auto loan offerings, exploring interest rates, application processes, repayment options, eligibility criteria, and customer experiences. We’ll compare GECU to its competitors, examine associated fees, and answer frequently asked questions to help you make an informed decision.

From understanding the factors influencing interest rates to navigating the application process and exploring various repayment options, we aim to provide a clear and concise overview of everything you need to know about securing a GECU auto loan. Whether you’re buying a new or used car, or refinancing an existing loan, this guide serves as your one-stop resource for navigating the intricacies of GECU’s auto loan programs.

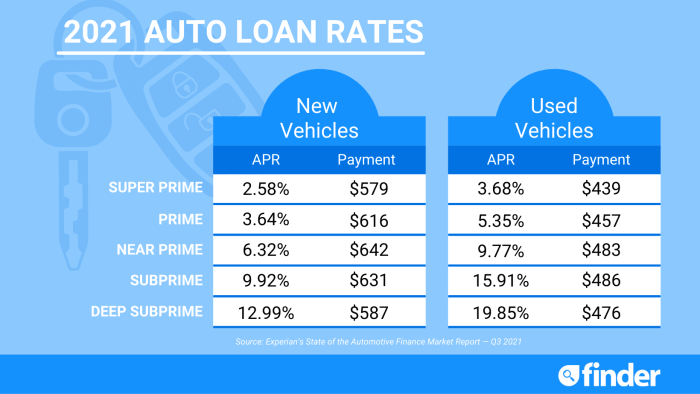

GECU Auto Loan Interest Rates: Gecu Auto Loans

Securing an auto loan involves careful consideration of interest rates, a crucial factor determining the overall cost of borrowing. Understanding the interest rates offered by GECU and comparing them to other financial institutions in the region is essential for making an informed decision. This section will analyze GECU’s auto loan interest rates, the factors influencing them, and the potential impact of broader economic trends.

GECU Auto Loan Interest Rates Compared to Competitors

The following table compares GECU’s auto loan interest rates to those of other major credit unions and banks. Note that interest rates are subject to change and are based on current market conditions and individual creditworthiness. The data presented here is for illustrative purposes and should not be considered a definitive representation of all available rates. Always check with the lender directly for the most up-to-date information.

| Lender | Loan Type | APR (Example Range) | Minimum Credit Score (Example Range) |

|---|---|---|---|

| GECU | New Car Loan | 3.99% – 14.99% | 660 – 780+ |

| Competitor A (Credit Union) | New Car Loan | 4.49% – 15.99% | 680 – 800+ |

| Competitor B (Bank) | Used Car Loan | 5.99% – 17.99% | 650 – 750+ |

| Competitor C (Credit Union) | Used Car Loan | 4.99% – 16.99% | 670 – 790+ |

Factors Influencing GECU Auto Loan Interest Rates

Several factors significantly influence the interest rate a borrower receives from GECU on an auto loan. These include:

- Credit Score: A higher credit score typically qualifies a borrower for a lower interest rate. Lenders view a higher score as an indication of lower risk.

- Loan Term: Longer loan terms generally result in higher interest rates due to the increased risk for the lender over a longer period.

- Vehicle Type: The type of vehicle being financed (new or used) can impact the interest rate. New cars often command lower rates due to their perceived higher value and lower risk of depreciation.

- Loan Amount: Larger loan amounts might carry slightly higher rates, reflecting a greater financial risk for the lender.

- Down Payment: A larger down payment can lead to a lower interest rate, as it reduces the loan amount and the lender’s risk.

Impact of Rising Interest Rates on GECU Auto Loan Costs

Rising interest rates in the broader economy directly affect auto loan costs. When interest rates increase, lenders typically adjust their rates upwards to reflect the increased cost of borrowing money. This means that borrowers applying for a GECU auto loan during a period of rising rates may face higher monthly payments and a greater overall cost of financing compared to borrowers who secured loans during a period of lower rates. For example, a 1% increase in the interest rate on a $25,000 loan over 60 months could result in an increase of several hundred dollars in total interest paid over the life of the loan. This increase can be substantial, emphasizing the importance of understanding the prevailing interest rate environment before committing to a loan.

GECU Auto Loan Application Process

Applying for a GECU auto loan involves a straightforward process designed for efficiency and transparency. Understanding the steps involved, from gathering necessary documents to loan approval, can significantly streamline your experience. This section details the application procedure and offers tips to increase your chances of approval.

The application process is designed to be user-friendly, whether you apply online or in person. GECU provides various channels to accommodate different preferences, making the process accessible to a wide range of applicants.

Steps in the GECU Auto Loan Application Process

The GECU auto loan application progresses through several key stages. Careful attention to each step will help ensure a smooth and timely application process.

- Pre-qualification: Begin by checking your pre-qualification eligibility online or contacting GECU directly. This step provides an initial assessment of your loan eligibility without impacting your credit score.

- Application Submission: Complete the formal application, either online through the GECU website or in person at a branch. Provide accurate and complete information.

- Document Submission: Gather and submit all required documentation (detailed below). Incomplete applications can delay the process.

- Credit Check: GECU will perform a credit check to assess your creditworthiness. A strong credit history improves your chances of approval.

- Vehicle Appraisal (if applicable): For used vehicles, GECU may require an appraisal to determine the vehicle’s value.

- Loan Approval/Denial: GECU will review your application and notify you of their decision. If approved, you’ll receive loan terms and details.

- Loan Closing: Once you accept the loan terms, you’ll complete the final paperwork and receive the funds.

Gathering Necessary Documentation for a GECU Auto Loan Application

Having the necessary documentation readily available significantly speeds up the application process. Ensure all documents are accurate and up-to-date to avoid delays.

- Valid Government-Issued Identification: Driver’s license or passport.

- Proof of Income: Pay stubs, tax returns, or bank statements showing consistent income.

- Proof of Residence: Utility bill or bank statement showing your current address.

- Vehicle Information: Vehicle Identification Number (VIN), make, model, and year. For used vehicles, a title or purchase agreement is necessary.

- Insurance Information: Proof of auto insurance coverage.

Tips for Improving GECU Auto Loan Approval Chances

Taking proactive steps can significantly improve your chances of securing a GECU auto loan. These strategies focus on demonstrating creditworthiness and financial responsibility.

- Maintain a Good Credit Score: A higher credit score significantly increases your approval odds and may result in more favorable interest rates. Regularly check your credit report and address any inaccuracies.

- Demonstrate Stable Income: Consistent employment history and stable income demonstrate your ability to repay the loan. Provide thorough documentation of your income.

- Manage Debt Wisely: Keep your debt-to-income ratio low. This shows lenders that you can manage your finances effectively.

- Shop Around for Rates: Comparing interest rates from different lenders can help you secure the best possible terms.

- Accurate Application: Provide complete and accurate information on your application to avoid delays or rejections.

GECU Auto Loan Repayment Options

Choosing the right repayment plan for your GECU auto loan is crucial for managing your finances effectively. Understanding the available options, including term lengths and payment frequencies, will allow you to select a plan that best suits your budget and financial goals. Careful consideration of these factors can significantly impact your overall loan cost.

GECU offers a range of repayment options to accommodate diverse financial situations. These options typically vary in terms of loan term length, influencing the monthly payment amount and the total interest paid over the life of the loan. Shorter loan terms generally result in higher monthly payments but lower overall interest costs, while longer terms offer lower monthly payments but higher overall interest costs. The frequency of payments is usually monthly, providing a predictable and manageable repayment schedule.

GECU Auto Loan Repayment Schedule Examples

The following table illustrates example repayment schedules for different loan terms. Remember that these are examples only, and your actual monthly payment will depend on the loan amount, interest rate, and chosen term length. It is always advisable to contact GECU directly to obtain a personalized quote based on your specific circumstances.

| Term Length (Years) | Monthly Payment Example | Total Interest Paid (Estimate) | Total Loan Cost (Estimate) |

|---|---|---|---|

| 3 | $500 | $3,000 | $18,000 |

| 4 | $375 | $4,000 | $19,000 |

| 5 | $300 | $5,000 | $20,000 |

| 6 | $250 | $6,000 | $21,000 |

Disclaimer: The figures presented in this table are for illustrative purposes only and are not a guarantee of actual loan terms. Interest rates and monthly payments are subject to change based on GECU’s lending criteria and prevailing market conditions. Contact GECU for current rates and personalized loan quotes.

Consequences of Late or Missed Payments

Late or missed payments on a GECU auto loan can have several significant negative consequences. These consequences can impact your credit score, potentially leading to higher interest rates on future loans. Furthermore, GECU may charge late payment fees, adding to the overall cost of your loan. In more severe cases, repeated late payments could lead to repossession of the vehicle. It’s crucial to adhere to the agreed-upon repayment schedule to avoid these negative repercussions.

Sample Repayment Schedule

This example demonstrates a simplified repayment schedule for a $15,000 GECU auto loan with a 5% annual interest rate over a 36-month term. Actual schedules will vary depending on the loan terms and interest rate.

| Month | Beginning Balance | Payment | Interest | Principal | Ending Balance |

|---|---|---|---|---|---|

| 1 | $15,000.00 | $446.30 | $62.50 | $383.80 | $14,616.20 |

| 2 | $14,616.20 | $446.30 | $60.90 | $385.40 | $14,230.80 |

| 3 | $14,230.80 | $446.30 | $59.28 | $387.02 | $13,843.78 |

| … | … | … | … | … | … |

| 36 | $446.30 | $446.30 | $1.86 | $444.44 | $0.00 |

Note: This is a simplified example and does not include any potential fees. The actual repayment schedule will be provided by GECU upon loan approval.

GECU Auto Loan Types and Eligibility

GECU offers a range of auto loan options to suit various needs and financial situations. Understanding the different loan types and their associated eligibility requirements is crucial for borrowers to select the most appropriate financing solution. This section details the various GECU auto loan types and Artikels the eligibility criteria for each.

GECU Auto Loan Types

GECU provides several auto loan types, catering to diverse borrowing needs. These typically include new car loans, used car loans, and refinancing options. New car loans are designed for the purchase of brand new vehicles directly from dealerships. Used car loans facilitate the financing of pre-owned vehicles. Refinancing allows borrowers to potentially secure a lower interest rate or better terms on an existing auto loan. Specific details regarding available loan types and their features may be subject to change, so confirming directly with GECU is always recommended.

GECU Auto Loan Eligibility Criteria

Eligibility criteria for GECU auto loans vary depending on the type of loan and the borrower’s financial profile. Generally, factors considered include credit score, income, debt-to-income ratio, and the vehicle’s value. Meeting the minimum requirements doesn’t guarantee approval; the final decision rests with GECU’s underwriting process.

GECU Auto Loan Type Comparison

The following table compares the different GECU auto loan types, highlighting their eligibility requirements, interest rate ranges, and loan term options. Note that interest rates and loan term options are subject to change based on prevailing market conditions and individual borrower circumstances. These ranges are for illustrative purposes only and should not be considered guaranteed rates. Always consult GECU for the most current information.

| Loan Type | Eligibility Requirements | Interest Rate Range (Example) | Loan Term Options (Example) |

|---|---|---|---|

| New Car Loan | Good to excellent credit score, sufficient income, acceptable debt-to-income ratio, valid driver’s license. | 3.00% – 8.00% APR | 24, 36, 48, 60, 72 months |

| Used Car Loan | Fair to excellent credit score, sufficient income, acceptable debt-to-income ratio, vehicle appraisal meeting GECU’s requirements, valid driver’s license. | 4.00% – 10.00% APR | 24, 36, 48, 60 months |

| Refinancing | Existing auto loan with a lender other than GECU, acceptable credit score, sufficient income, acceptable debt-to-income ratio. | Variable, depending on credit score and existing loan terms. | Variable, depending on existing loan terms. |

GECU Auto Loan Customer Reviews and Experiences

Understanding customer feedback is crucial for assessing the overall quality and effectiveness of GECU’s auto loan services. Analyzing reviews from various online platforms provides valuable insights into customer satisfaction and areas for potential improvement. This section summarizes customer reviews and experiences, highlighting common themes and providing illustrative examples. It is important to note that individual experiences can vary.

Summary of Customer Reviews

Customer reviews regarding GECU auto loans are mixed, reflecting the diverse experiences of borrowers. A comprehensive analysis of reviews from platforms like Google Reviews, Yelp, and the Better Business Bureau reveals both positive and negative aspects of the service. The following points categorize this feedback.

- Positive Feedback: Many customers praise GECU’s competitive interest rates, efficient application process, and helpful customer service representatives. Several reviewers highlight the ease of online account management and the flexibility offered in repayment options.

- Negative Feedback: Some negative reviews cite difficulties in reaching customer service representatives, long wait times for loan approvals, and challenges in modifying loan terms. A few reviewers express dissatisfaction with the overall communication process.

Common Themes in Customer Feedback

Several recurring themes emerge from the analysis of GECU auto loan customer reviews. These themes provide a clearer picture of both the strengths and weaknesses of the service.

- Interest Rates and Fees: A significant portion of positive reviews focus on the competitiveness of GECU’s interest rates. Conversely, some negative feedback mentions hidden fees or unexpected charges.

- Customer Service: The quality of customer service is a recurring theme, with some customers praising the helpfulness and responsiveness of GECU representatives, while others report difficulties in reaching representatives or experiencing unhelpful interactions.

- Application and Approval Process: Reviews highlight both the speed and efficiency of the application process for some borrowers, while others report lengthy wait times for loan approvals and unclear communication throughout the process.

Examples of Customer Experiences

To illustrate the range of customer experiences, we present anonymized examples.

- Positive Experience: “I recently secured an auto loan through GECU and the entire process was seamless. The interest rate was excellent, and the staff were incredibly helpful and responsive to all my questions. I highly recommend their services.”

- Negative Experience: “I had a frustrating experience trying to reach someone at GECU regarding my loan. I spent hours on hold and still didn’t get the answers I needed. The communication throughout the process was poor.”

Comparing GECU Auto Loans with Competitors

Choosing the right auto loan can significantly impact your overall cost. Understanding the differences between lenders is crucial for securing the best possible terms. This section compares GECU auto loans with those of three major competitors, highlighting key advantages and disadvantages to aid in your decision-making process. We will analyze interest rates, loan term options, and associated fees to provide a comprehensive comparison.

GECU Auto Loan Comparison with Competitors

The following table compares GECU’s auto loan offerings with those of three representative competitors: Capital One Auto Navigator, USAA, and Navy Federal Credit Union. Note that interest rates and fees are subject to change and are based on typical offers at the time of writing. Individual rates will vary depending on credit score, loan amount, and other factors.

| Lender | Interest Rate (Example APR) | Loan Term Options (Years) | Fees |

|---|---|---|---|

| GECU | Variable, depending on creditworthiness; Example: 6.5% – 15% | 24, 36, 48, 60, 72, 84 | Potential origination fee; check with GECU for current details. |

| Capital One Auto Navigator | Variable, depending on creditworthiness; Example: 7% – 18% | 24, 36, 48, 60, 72 | Potential origination fee; check with Capital One for current details. |

| USAA | Variable, depending on creditworthiness; Example: 6% – 17% | 24, 36, 48, 60, 72 | Potential origination fee; check with USAA for current details. |

| Navy Federal Credit Union | Variable, depending on creditworthiness; Example: 5.5% – 16% | 24, 36, 48, 60, 72, 84 | Potential origination fee; check with Navy Federal for current details. |

Advantages and Disadvantages of GECU Auto Loans

Choosing a lender involves weighing various factors. GECU, as a credit union, often emphasizes member benefits and potentially offers personalized service. However, its loan availability might be limited geographically compared to national lenders like Capital One.

Advantages of GECU: Potential for lower rates for members with good credit, personalized service, and community focus.

Disadvantages of GECU: Limited geographical reach; may have stricter eligibility requirements than some national lenders.

Advantages of Competitors: Wider geographical reach, potentially more flexible loan options, extensive online tools.

Disadvantages of Competitors: Potentially higher interest rates for borrowers with less-than-perfect credit, less personalized service, focus on profit maximization over member benefits (for banks, not credit unions).

Factors to Consider When Comparing Auto Loan Offers

Consumers should carefully compare several key aspects before selecting an auto loan. This includes the Annual Percentage Rate (APR), which reflects the total cost of borrowing, including interest and fees. Loan term length affects monthly payments and the total interest paid over the life of the loan. A shorter term means higher monthly payments but lower total interest, while a longer term means lower monthly payments but higher total interest. Finally, understanding all associated fees, such as origination fees or prepayment penalties, is crucial for accurately assessing the overall cost. Consider your credit score, as this significantly impacts the interest rate you qualify for. Pre-qualifying with multiple lenders allows for comparison shopping without impacting your credit score.

GECU Auto Loan Fees and Charges

Understanding the fees associated with a GECU auto loan is crucial for accurately budgeting and comparing loan options. These fees, while seemingly small individually, can significantly impact the overall cost of borrowing over the loan’s lifespan. Failing to account for these charges can lead to unexpected expenses and a higher total repayment amount.

GECU, like most financial institutions, charges various fees associated with their auto loans. These fees are typically disclosed upfront in the loan agreement, but it’s essential to thoroughly review them before signing. Understanding these fees allows for a more informed decision and a clearer picture of the true cost of the loan.

Types of GECU Auto Loan Fees, Gecu auto loans

Several fees can be associated with a GECU auto loan. It’s important to note that the specific fees and their amounts may vary depending on the loan type, creditworthiness, and the terms of the agreement. Always confirm the applicable fees directly with GECU.

- Origination Fee: This fee covers the administrative costs associated with processing your loan application. It’s typically a percentage of the loan amount or a fixed dollar amount.

- Prepayment Penalty: This fee is charged if you pay off your loan early. It can vary depending on the loan terms and how early you repay. Some loans may not have a prepayment penalty.

- Late Payment Fee: A fee assessed if you miss a scheduled payment. The amount of the late fee is usually specified in the loan agreement.

- Returned Check Fee: This fee is incurred if a payment check is returned due to insufficient funds.

- Document Preparation Fee: A fee for preparing and processing the necessary loan documentation.

Impact of Fees on Overall Loan Cost

The cumulative effect of these fees can significantly increase the total cost of your auto loan. Even seemingly small fees, when compounded over the loan term, can add hundreds or even thousands of dollars to the total amount repaid. For example, a 1% origination fee on a $20,000 loan is $200, while a $50 late payment fee, if incurred multiple times, can easily reach $200 or more.

Calculating Total Loan Cost

To accurately calculate the total cost of your GECU auto loan, you need to factor in all applicable fees alongside the principal loan amount and interest. This can be done using a loan amortization calculator, readily available online. Many calculators allow you to input the loan amount, interest rate, loan term, and all associated fees to determine the total amount you will repay.

Total Loan Cost = Principal Loan Amount + Total Interest Paid + Origination Fee + Prepayment Penalty (if applicable) + Late Payment Fees (if applicable) + Other Fees

For example, consider a $20,000 auto loan with a 5% interest rate over 60 months, a $200 origination fee, and a potential $50 late payment fee (incurred twice). Using a loan amortization calculator, including these fees, will provide a precise total cost. Without including the fees, the calculation would underestimate the true cost of the loan.

Closing Notes

Securing an auto loan can be a significant financial undertaking. By carefully considering factors like interest rates, loan terms, fees, and your own financial situation, you can make an informed choice that best suits your needs. This guide has provided a detailed exploration of GECU auto loans, equipping you with the knowledge to compare options, understand the application process, and ultimately, make a confident decision about your car financing. Remember to always review the fine print and compare offers from multiple lenders before committing to a loan.

FAQ Guide

What credit score is needed for a GECU auto loan?

While GECU doesn’t publicly state a minimum credit score, a higher score generally leads to better interest rates. It’s best to check your credit report and contact GECU directly for specifics.

Can I pre-qualify for a GECU auto loan online?

GECU’s website may offer pre-qualification tools. However, a formal application is usually required for final approval and loan terms.

What types of vehicles are eligible for GECU auto loans?

GECU typically offers loans for new and used cars, trucks, SUVs, and motorcycles. Specific eligibility may vary; check with GECU for details.

What happens if I miss a payment on my GECU auto loan?

Late payments can result in late fees, damage to your credit score, and potential repossession of the vehicle. Contact GECU immediately if you anticipate difficulty making a payment.