Kemba auto loan rates are a key consideration for anyone seeking financing for a new or used vehicle. Understanding these rates, the factors influencing them, and the application process is crucial for securing the best possible loan terms. This guide delves into the specifics of Kemba’s auto loan offerings, providing a comprehensive overview of interest rates, influencing factors, the application process, and essential terms and conditions. We’ll also explore how to manage your loan effectively and what resources are available for customer support.

From comparing current interest rates across various loan terms and amounts to examining the impact of your credit score, this resource aims to empower you with the knowledge needed to make informed decisions about your Kemba auto loan. We’ll explore the application process step-by-step, highlight key terms and conditions, and offer practical advice for managing your loan effectively.

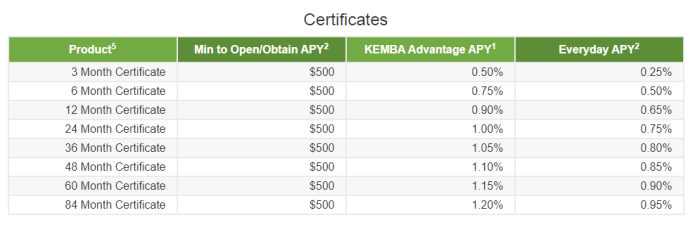

Kemba Auto Loan Interest Rates

Kemba Credit Union offers a range of auto loan options with varying interest rates and terms. Understanding these rates is crucial for borrowers to make informed decisions and secure the best financing for their vehicle purchase. The rates offered are competitive and depend on several factors, including credit score, loan term, and the type of vehicle being financed. This section will detail Kemba’s current auto loan interest rates, providing examples to illustrate the cost of borrowing.

Kemba’s Current Auto Loan Interest Rate Offers

Kemba’s auto loan interest rates are not publicly listed on a single, easily accessible page. Rates are determined individually based on a creditworthiness assessment. However, we can provide a representative range based on industry averages and typical Kemba offerings. It’s important to contact Kemba directly for the most up-to-date and personalized rate quotes. Keep in mind that these are estimates and your actual rate may vary.

Sample Auto Loan Payment Calculations

The following table provides examples of monthly payments for various loan amounts, terms, and interest rates. These are illustrative examples and should not be considered guarantees of actual rates or payments. Remember that factors such as your credit score and the type of vehicle significantly impact your final interest rate.

| Loan Amount | Loan Term (Months) | Interest Rate (APR) | Monthly Payment (Estimate) |

|---|---|---|---|

| $20,000 | 36 | 5.00% | $591 |

| $20,000 | 60 | 6.00% | $387 |

| $30,000 | 72 | 7.00% | $500 |

| $15,000 | 48 | 4.50% | $343 |

Special Offers and Promotions

Kemba frequently offers special promotions on auto loans, such as reduced interest rates for members who meet specific criteria, or incentives for financing new or used vehicles from participating dealerships. These promotions can vary throughout the year. To learn about any current special offers, it’s recommended to visit a Kemba branch, call their customer service line, or check their official website. These promotions often have limited-time availability and specific eligibility requirements. Contacting Kemba directly is the best way to stay informed about any current deals.

Factors Influencing Kemba Auto Loan Rates

Securing an auto loan involves understanding the factors that determine the interest rate you’ll receive. Several key elements influence the final rate offered by Kemba Credit Union, impacting your monthly payments and overall loan cost. This section details those crucial factors and their effect on your Kemba auto loan.

Your Kemba auto loan interest rate is not arbitrarily assigned; rather, it’s a calculation based on a comprehensive assessment of your financial profile and the loan specifics. A lower interest rate translates to lower monthly payments and less interest paid over the life of the loan, making it a crucial factor to consider when seeking financing.

Credit Score’s Impact on Interest Rates

Your credit score is arguably the most significant factor determining your Kemba auto loan interest rate. Lenders use credit scores to assess your creditworthiness – your ability to repay borrowed money responsibly. A higher credit score indicates a lower risk to the lender, resulting in a more favorable interest rate. Conversely, a lower credit score signals a higher risk, leading to a higher interest rate to compensate for that increased risk. For example, a borrower with a credit score above 750 might qualify for a significantly lower interest rate than someone with a score below 600. Credit reports from agencies like Experian, Equifax, and TransUnion are used to calculate the score, considering factors such as payment history, amounts owed, length of credit history, and new credit.

Loan Amount, Term, and Vehicle Type

The amount you borrow, the loan term, and the type of vehicle you’re financing all play a role in shaping your interest rate. Larger loan amounts generally carry slightly higher interest rates due to the increased risk for the lender. Longer loan terms, while resulting in lower monthly payments, often come with higher overall interest costs because you’re paying interest for a longer period. The vehicle type itself can also influence the rate; newer vehicles with higher resale value may be associated with lower interest rates compared to older vehicles or those with lower resale potential. This is because the lender views the vehicle as a more secure asset in case of default.

Comparison with Other Major Lenders

While specific interest rates vary constantly based on market conditions and individual borrower profiles, it’s important to compare Kemba’s offerings with other major auto lenders. Direct comparison requires checking current rates from each lender, which fluctuate frequently. However, generally, credit unions like Kemba often offer competitive rates, sometimes lower than those from large banks or online lenders. This advantage stems from their member-focused approach and often non-profit structure, allowing them to prioritize member benefits over maximizing profit margins. However, it’s crucial to obtain personalized quotes from multiple lenders to ensure you’re securing the best possible rate for your individual circumstances.

Kemba Auto Loan Application Process

Securing a Kemba auto loan involves a straightforward process designed for efficiency and transparency. Understanding the steps involved can significantly streamline your application and increase your chances of approval. This section Artikels the key stages, from initial inquiry to final loan disbursement.

The Kemba auto loan application process is designed to be user-friendly, guiding applicants through each step with clear instructions and readily available support. Applicants should gather all necessary documentation beforehand to expedite the process.

Required Documentation and Information

Before initiating the application, gather the necessary documentation. This will expedite the review process and minimize potential delays. Having all the required materials ready ensures a smooth and efficient application.

- Valid Driver’s License or State-Issued ID: This verifies your identity and residency.

- Proof of Income: Pay stubs, tax returns, or bank statements demonstrating consistent income are essential to establish your repayment capacity. This could include W-2 forms, 1099s, or recent pay stubs showing at least three months of income.

- Proof of Residence: Utility bills, rental agreements, or mortgage statements confirming your current address are required.

- Vehicle Information: Details about the vehicle you intend to purchase, including the Year, Make, Model, VIN (Vehicle Identification Number), and mileage. A copy of the vehicle’s title may also be required.

- Credit Report Information: While Kemba will obtain your credit report, providing pre-approval information, if available, can be helpful.

Application Submission and Review

Submitting your application marks the formal commencement of the loan process. Kemba offers various application methods, ensuring convenience for applicants.

- Online Application: Kemba’s user-friendly online portal allows for quick and convenient application submission. Applicants can complete the form, upload necessary documents, and track the progress of their application online.

- In-Person Application: Applicants can visit a local Kemba branch to apply in person with the assistance of a loan officer. This allows for immediate clarification of any questions and personalized guidance.

- Phone Application: For those who prefer a phone-based approach, Kemba provides dedicated loan officers to assist with the application process over the phone. This method allows for a more personalized experience and direct interaction with a loan specialist.

Loan Approval and Disbursement

Following application review, Kemba will notify you of the decision. Upon approval, funds are typically disbursed quickly.

- Credit Check and Approval: Kemba will review your application, including your credit score and financial history, to assess your creditworthiness and determine the loan terms.

- Loan Offer: Upon approval, Kemba will present a loan offer outlining the interest rate, loan term, and monthly payment amount. Carefully review the terms before accepting the offer.

- Loan Documentation and Signing: Once you accept the loan offer, you will need to sign the necessary loan documents. These documents will Artikel the terms and conditions of the loan agreement.

- Loan Disbursement: After signing the loan documents, Kemba will disburse the loan funds, typically directly to the vehicle seller or to your account.

Understanding Kemba Auto Loan Terms and Conditions

Kemba Credit Union offers various auto loan options, each with its own set of terms and conditions. Understanding these terms is crucial before committing to a loan, as they directly impact your monthly payments and overall cost. Failure to adhere to these conditions can result in penalties and potentially damage your credit score. This section will detail the key aspects of Kemba’s auto loan agreements, focusing on the different loan types and common stipulations.

Types of Kemba Auto Loans

Kemba likely offers several types of auto loans catering to different needs and financial situations. These typically include new car loans for the purchase of brand-new vehicles and used car loans for pre-owned vehicles. The interest rates and loan terms may vary depending on the type of loan and the borrower’s creditworthiness. New car loans might offer lower interest rates due to the lower risk associated with newer vehicles, while used car loans may have higher rates reflecting the increased risk. Specific details regarding available loan types and their associated terms should be confirmed directly with Kemba Credit Union.

Common Terms and Conditions of Kemba Auto Loans

Kemba’s auto loan agreements likely include several standard terms and conditions. These commonly involve prepayment penalties, late payment fees, and insurance requirements. Prepayment penalties are fees charged if you pay off the loan early, designed to compensate the lender for lost interest income. Late payment fees are incurred if payments are not made by the due date, and these fees can significantly increase the overall cost of the loan. Insurance requirements usually mandate maintaining comprehensive and collision insurance on the financed vehicle throughout the loan term, protecting the lender’s investment. The exact amounts of these fees and the specifics of the insurance requirements will be detailed in the loan agreement.

Examples of Key Clauses in a Typical Kemba Auto Loan Agreement

A typical Kemba auto loan agreement would include clauses outlining the loan amount, interest rate, loan term (duration), monthly payment amount, payment due date, and any applicable fees. For example, a clause might state: “The borrower agrees to pay a monthly installment of $X on the Yth of each month, for a period of Z months, at an annual interest rate of A%.” Another clause might specify: “A late payment fee of $B will be charged for any payment received after the due date.” A third clause could detail the prepayment penalty: “Prepayment of the loan within the first N months will incur a penalty equal to C% of the outstanding loan balance.” It’s vital to carefully review all clauses in the loan agreement before signing to fully understand your obligations. Note that these are examples and the specific wording and amounts will vary based on the individual loan agreement. Obtaining a sample loan agreement directly from Kemba is recommended for a complete understanding.

Managing Kemba Auto Loans

Effectively managing your Kemba auto loan is crucial for maintaining a healthy financial standing and avoiding potential penalties. Proactive strategies and careful tracking of your loan details will help you stay on top of payments and protect your credit score. This section Artikels practical steps and methods for successful loan management.

Successful auto loan management involves a combination of proactive planning, diligent record-keeping, and understanding your loan terms. By implementing the strategies described below, you can minimize the risk of late payments and ensure a smooth repayment process. This not only safeguards your credit score but also reduces the overall cost of borrowing.

Auto Loan Payment Management Strategies

Avoiding late payments is paramount for maintaining a good credit score. Consistent on-time payments significantly impact your creditworthiness. Here are key strategies to ensure timely payments.

- Set up automatic payments: Automating your payments through online banking or direct debit eliminates the risk of forgetting a payment deadline. This ensures consistent and timely payments, preventing late fees and negative impacts on your credit report.

- Budgeting and financial planning: Integrate your loan payment into your monthly budget. Track your income and expenses to ensure you have sufficient funds available each month for the payment. Unexpected expenses should be anticipated and accounted for.

- Payment reminders: Set calendar reminders or use budgeting apps to receive notifications before your payment is due. This serves as an additional layer of protection against missed payments.

- Communicate with Kemba: If you anticipate difficulty making a payment, contact Kemba immediately. They may offer options such as payment extensions or hardship programs to help you avoid delinquency.

Auto Loan Record-Keeping Best Practices

Maintaining organized records of your Kemba auto loan is essential for tracking payments, understanding interest accrual, and resolving any potential discrepancies. A well-maintained record simplifies the loan management process.

- Keep a copy of your loan agreement: This document contains all the essential details of your loan, including the interest rate, repayment schedule, and any applicable fees.

- Maintain a payment log: Record each payment made, including the date, amount, and payment method. This helps track your payment history and easily identify any potential discrepancies.

- Store all loan-related documents securely: Keep your loan agreement, payment confirmations, and other relevant documents in a safe and accessible location, either physically or digitally.

- Regularly review your loan statement: Review your monthly statement to ensure accuracy and identify any potential errors or discrepancies promptly.

Calculating Monthly Payments and Accrued Interest

Understanding how your monthly payment is calculated and how much interest you are paying is crucial for effective loan management. Several methods can be used to calculate these figures.

The most common method for calculating monthly payments uses the following formula:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Number of Months in Loan Term

For example, a $20,000 loan at 5% annual interest over 60 months would result in a monthly payment of approximately $377.42. Accrued interest can be calculated by subtracting the principal paid from the total amount paid over a specific period.

Many online calculators and loan amortization schedules are available to simplify these calculations. Using these tools can provide a clear picture of your payment schedule and interest accrual over the life of the loan.

Kemba Auto Loan Customer Service and Support

Kemba Credit Union prioritizes providing excellent customer service to its auto loan borrowers. Understanding the various support channels available and how to effectively utilize them is crucial for a smooth and positive borrowing experience. This section details the methods Kemba offers for addressing inquiries and resolving issues related to auto loans.

Accessing Kemba’s customer support is straightforward and designed for convenience. Multiple channels are available to suit individual preferences and needs. Effective communication is key to resolving any concerns quickly and efficiently.

Contacting Kemba Customer Support, Kemba auto loan rates

Kemba offers several avenues for contacting their customer support team regarding auto loans. These options provide flexibility for borrowers to choose the method most convenient for them. Direct communication with a representative ensures personalized assistance and timely resolution of issues.

- Phone Support: Kemba provides a dedicated phone number for auto loan inquiries. This allows for immediate assistance and the ability to speak directly with a representative. The phone number is typically prominently displayed on their website and loan documents.

- Email Support: For non-urgent inquiries or to provide documentation, email support is a valuable option. Borrowers can compose a detailed message outlining their question or concern, including relevant account information. Response times may vary depending on the complexity of the issue and the volume of inquiries.

- Online Resources: Kemba’s website likely features a comprehensive FAQ section addressing common auto loan questions. This self-service resource can quickly resolve many simple inquiries without the need for direct contact. Online account access may also allow borrowers to view statements, make payments, and track loan progress.

- In-Person Support: Depending on location, borrowers may be able to visit a Kemba branch in person for assistance. This offers a face-to-face interaction, particularly beneficial for complex issues requiring detailed explanation or documentation review.

Common Customer Service Issues and Resolutions

Many common issues arise during the auto loan process. Understanding these issues and the steps to resolve them can significantly improve the overall borrowing experience. Proactive problem-solving can prevent minor inconveniences from escalating into larger problems.

- Payment Issues: Missed or late payments can lead to penalties. Contacting Kemba immediately to discuss payment arrangements is crucial. They may offer options such as payment extensions or alternative payment methods to avoid negative consequences.

- Loan Modification Requests: Circumstances change, and borrowers may need to modify their loan terms. Contacting Kemba to discuss potential modifications, such as extending the loan term or adjusting the payment schedule, is recommended. They will assess the request and determine feasibility.

- Account Inquiries: Questions about loan balances, payment history, or interest rates can be easily resolved by contacting Kemba’s customer support. They can provide detailed information and clarify any discrepancies.

- Dispute Resolution: If a borrower believes there is an error on their account, they should promptly contact Kemba to initiate a dispute resolution process. Providing supporting documentation will expedite the resolution.

- Technical Issues with Online Account Access: Difficulties accessing online accounts should be reported to Kemba’s customer support. They can troubleshoot the issue, provide technical assistance, or reset passwords as needed.

Outcome Summary

Securing a Kemba auto loan requires careful planning and understanding of the associated rates and terms. By thoroughly researching the factors influencing your interest rate, completing the application process diligently, and proactively managing your loan, you can navigate the process successfully. Remember to leverage Kemba’s customer support resources if you encounter any questions or challenges. This guide provides a solid foundation for making informed decisions and achieving your automotive financing goals with Kemba.

FAQ Summary: Kemba Auto Loan Rates

What credit score is needed for a favorable Kemba auto loan rate?

While Kemba doesn’t publicly state a minimum credit score, a higher credit score generally results in a lower interest rate. Aim for a score above 700 for the best chances of securing a competitive rate.

Can I refinance my existing auto loan with Kemba?

Yes, Kemba may offer auto loan refinancing options. Contact their customer service to inquire about eligibility and current rates.

What types of vehicles are eligible for Kemba auto loans?

Kemba typically finances new and used vehicles. Specific eligibility criteria may vary depending on the vehicle’s age, condition, and value. Contact Kemba for details.

What happens if I miss a payment on my Kemba auto loan?

Missing payments will negatively impact your credit score and may result in late fees. Contact Kemba immediately if you anticipate difficulty making a payment to explore potential solutions.